“When I was a black hat hacker, I was isolated and paranoid,” he wrote. “Working with the good guys, being part of a team solving a bigger problem felt surprisingly good. I realized that I could use my technical skills to make a difference.

Lichtenstein, who did not immediately respond to Ars’ request for comment, noted that he was sentenced to 60 months in prison and spent “nearly [four] years in some of the harshest jails in the country.” While in prison, Lichtenstein says that he spent as much time as he could in the prison library studying math books to engage his mind and distract himself from his surroundings.

The 38-year-old added that he was “released to home confinement earlier this month.”

Convicted hackers cooperating with federal authorities or turning their lives around is not without precedent.

One notable example is the late Kevin Mitnick, who was convicted of multiple phone and computer crime cases in the 1980s and 1990s. Mitnick eventually started his own security consulting company and became a penetration tester and public speaker for many years before his death in 2023.

“Now begins the real challenge of regaining the community’s trust,” Lichtenstein concluded, noting that he wants to work in cybersecurity.

“I think like an adversary,” he said. “I’ve been an adversary. Now I can use those same skills to stop the next billion-dollar hack.”

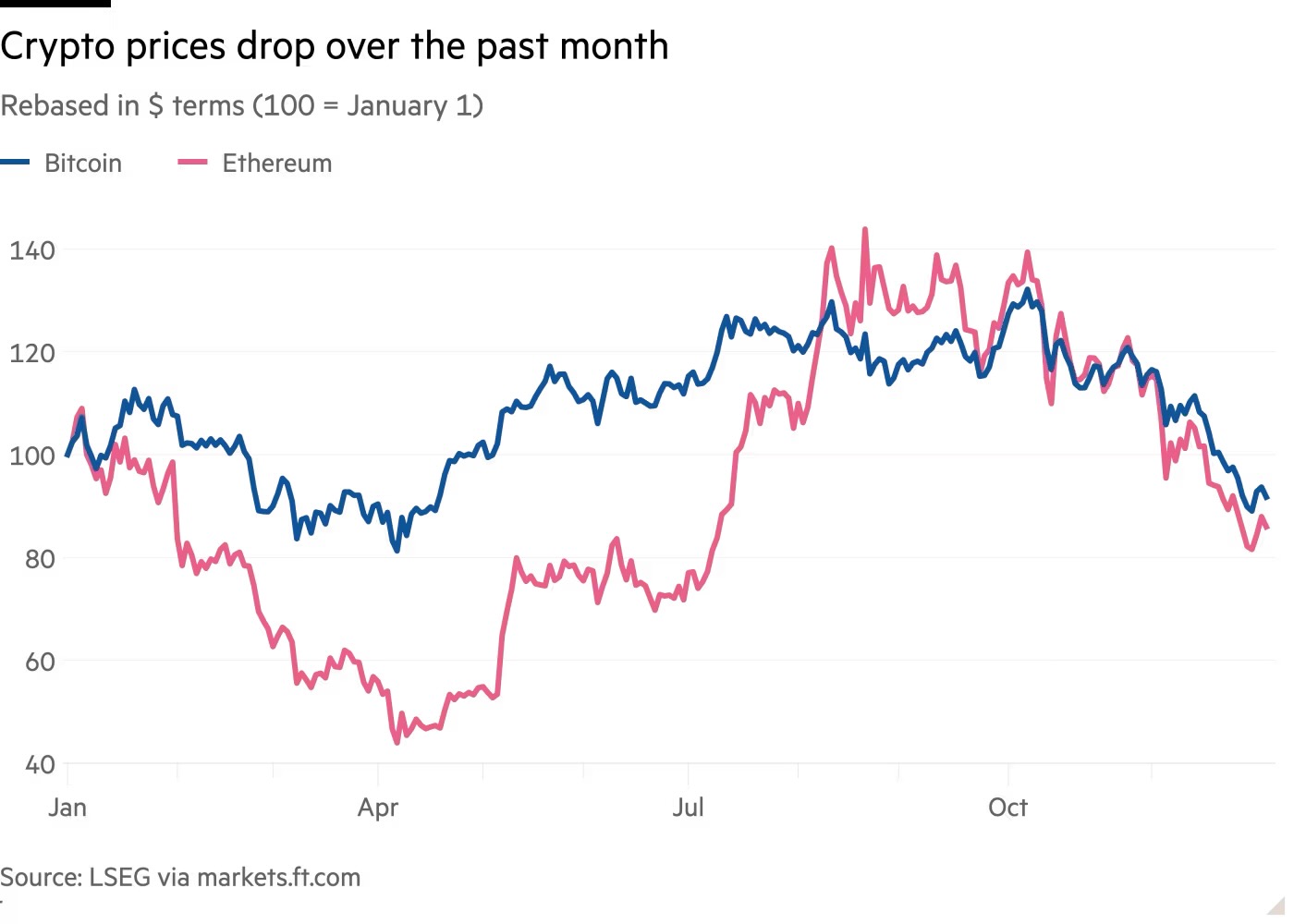

“It was inevitable,” said Jake Ostrovskis, head of OTC trading at Wintermute, referring to the sell-off in digital asset treasury stocks. “It got to the point where there’s too many of them.”

Several companies have begun selling their crypto stockpiles in an effort to fund share buybacks and shore up their stock prices, in effect putting the crypto treasury model into reverse.

North Carolina-based ether holder FG Nexus sold about $41.5 million of its tokens recently to fund its share buyback program. Its market cap is $104 million, while the crypto it holds is worth $116 million. Florida-based life sciences company turned ether buyer ETHZilla recently sold about $40 million worth of its tokens, also to fund its share buyback program.

Sequans Communications, a French semiconductor company, sold about $100 million of its bitcoin this month in order to service its debt, in a sign of how some companies that borrowed to fund crypto purchases are now struggling. Sequans’ market capitalization is $87 million, while the bitcoin it holds is worth $198 million.

Georges Karam, chief executive of Sequans, said the sale was a “tactical decision aimed at unlocking shareholder value given current market conditions.”

While bitcoin and ether sellers can find buyers, companies with more niche tokens will find it more difficult to raise money from their holdings, according to Morgan McCarthy. “When you’ve got a medical device company buying some long-tail asset in crypto, a niche in a niche market, it is not going to end well,” he said, adding that 95 percent of digital asset treasuries “will go to zero.”

Strategy, meanwhile, has doubled down and bought even more bitcoin as the price of the token has fallen to $87,000, from $115,000 a month ago. The firm also faces the looming possibility of being cut from some major equity indices, which could heap even more selling pressure on the stock.

But Saylor has brushed off any concerns. “Volatility is Satoshi’s gift to the faithful,” he said this week, referring to the pseudonymous creator of bitcoin.

Federal prosecutors have seized $15 billion from the alleged kingpin of an operation that used imprisoned laborers to trick unsuspecting people into making investments in phony funds, often after spending months faking romantic relationships with the victims.

Such “pig butchering” scams have operated for years. They typically work when members of the operation initiate conversations with people on social media and then spend months messaging them. Often, the scammers pose as attractive individuals who feign romantic interest for the victim.

Forced labor, phone farms, and human suffering

Eventually, conversations turn to phony investment funds with the end goal of convincing the victim to transfer large amounts of bitcoin. In many cases, the scammers are trafficked and held against their will in compounds surrounded by fences and barbed wire.

On Tuesday, federal prosecutors unsealed an indictment against Chen Zhi, the founder and chairman of a multinational business conglomerate based in Cambodia. It alleged that Zhi led such a forced-labor scam operation, which, with the help of unnamed co-conspirators, netted billions of dollars from victims.

“The defendant CHEN ZHI and his co-conspirators designed the compounds to maximize profits and personally ensured that they had the necessary infrastructure to reach as many victims as possible,” prosecutors wrote in the court document, filed in US District Court for the Eastern District of New York. The indictment continued:

For example, in or about 2018, Co-Conspirator-1 was involved in procuring millions of mobile telephone numbers and account passwords from an illicit online marketplace. In or about 2019, Co-Conspirator-3 helped oversee construction of the Golden Fortune compound. CHEN himself maintained documents describing and depicting “phone farms,” automated call centers used to facilitate cryptocurrency investment fraud and other cybercrimes, including the below image:

Credit: Justice Department

Prosecutors said Zhi is the founder and chairman of Prince Group, a Cambodian corporate conglomerate that ostensibly operated dozens of legitimate business entities in more than 30 countries. In secret, however, Zhi and top executives built Prince Group into one of Asia’s largest transnational criminal organizations. Zhi’s whereabouts are unknown.

Police have arrested a third suspect linked to one of the most extreme bitcoin-related kidnapping and torture cases in the United States, The New York Times reported.

The arrest came after an Italian man, Michael Valentino Teofrasto Carturan, escaped a luxury Manhattan townhouse after three weeks of alleged imprisonment.

Running to a traffic agent for help, he later told police that he was tortured by colleagues for his bitcoin password, “bound with electrical cords and whipped with a gun,” his feet submerged in water while a Taser gun sent jolts through his body, the NYT reported. At times he feared for his life—allegedly once held suspended from the ledge of the fifth-story building—but he seemingly never gave up his password, a resistance that only prompted more extreme violence.

Police raided the townhouse and found photos depicting the torture, as well as “several guns, a ballistic vest, and broken furniture,” the NYT reported. Two butlers onsite agreed to be interviewed. Cops soon after arrested two suspects—John Woeltz, 37, and Beatrice Folchi, 24—but were still seeking an “unapprehended male,” the NYT previously reported. Folchi was released after her prosecution was deferred, but Woeltz was held without bail after being charged with assault, kidnapping, unlawful imprisonment, and criminal possession of a gun, the NYT reported.

On Tuesday morning, 33-year-old William Duplessie surrendered to police after days of negotiations, Police Commissioner Jessica Tisch told the NYT. Like Woeltz, he faces charges of kidnapping and false imprisonment, Tisch confirmed.

According to Carturan, he met Woeltz through a crypto hedge fund in New York, but they quickly had a falling out over money, prompting Carturan to return home to Italy.

Ahead of the first-ever White House Crypto Summit Friday, President Donald Trump signed an executive order establishing a strategic bitcoin reserve that a factsheet claimed delivers on his promise to make America the “crypto capital of the world.”

Trump’s order requires all federal agencies currently holding bitcoins seized as part of a criminal or civil asset forfeiture proceeding to transfer those bitcoins to the Treasury Department, which itself already has a store of bitcoins. Additionally, any other digital assets forfeited will be collected in a separate Digital Assets Stockpile.

But while Trump likely anticipates that bitcoin fans will be over the moon about this news—his announcement of the reserve and looser crypto regulations helped send bitcoin’s price to its all-time high of $109,000 in January, Reuters noted—some cryptocurrency enthusiasts were clearly disappointed that Trump’s order confirmed that the US currently has no plans to buy any more bitcoins at this time.

Bitcoin’s price briefly dropped by about 5 percent to $85,000 on the news, Reuters reported. Charles Edwards, the founder of a bitcoin-focused hedge fund called Capriole Investments, took to X (formerly Twitter) to declare that Trump’s order is “a pig in lipstick.” Currently, bitcoin’s price is around $90,500.

“This is the most underwhelming and disappointing outcome we could have expected for this week,” Edwards wrote. “No active buying means this is just a fancy title for Bitcoin holdings that already existed” with the government.

A digital assets managing director at S&P Global Ratings, Andrew O’Neill, agreed, telling Reuters that the “significance” of Trump’s order was “mainly symbolic” and provides no timeline for when more bitcoin might be acquired by the US.

In the factsheet, the White House insisted that the strategic reserve and digital assets stockpile would harness “the power of digital assets for national prosperity rather than letting them languish in limbo.”

The price of bitcoin hit a record high of $109,114.88 during intraday trading on January 20, the day of President Trump’s inauguration, but has plummeted since and went as low as $83,741.94 during today’s trading.

That’s a 23.3 percent drop from the intraday record to today’s low, though it was back over $84,000 as of this writing. Bitcoin had been above $100,000 as recently as February 7, and was over $96,000 on Monday this week.

Bitcoin’s drop is part of a wider rout in which over $800 billion of nominal value “has been wiped off global cryptocurrency markets in recent weeks, as the enthusiasm that swept the crypto industry after Donald Trump’s election victory last year ebbs away,” the Financial Times wrote today.

Bitcoin hit a then-record of $89,623 in November, a week after the election, amid optimism about Trump’s plans for crypto-friendly policies. It hit $100,000 for the first time in early December after Trump announced his planned nomination of Paul Atkins to lead the Securities and Exchange Commission.

Trump made several early moves to support crypto. “After pouring tens of millions of dollars into Trump’s 2024 campaign for president, the crypto industry has been paid back handsomely during his first week in the White House,” CNBC wrote on January 25.

For example, the SEC rescinded a 2022 accounting rule “that forced banks to treat bitcoin and other tokens as a liability on their balance sheets,” a change that is said to make it easier for “regulated institutions to adopt crypto as an asset class that they support on behalf of the clients.”

Trump impact overestimated

But enthusiasm waned as crypto investors apparently expected Trump to do more to boost the market in the five weeks since his inauguration. Traders hoped the US would start buying bitcoin and “rapidly enact new rules to encourage large financial institutions to buy crypto,” today’s Financial Times article said.

“There has been a recalibration of expectations regarding the Trump administration’s crypto stance,” Gadi Chait, investment manager at Xapo Bank, told the Financial Times. Michael Dempsey, managing partner at venture capital firm Compound, was quoted as saying that many crypto enthusiasts “materially overestimated [Trump’s] positive impact on the space.”

At the end of 2024, a US court authorized the Department of Justice to sell 69,370 bitcoins from “the largest cryptocurrency seizure in history.”

At bitcoin’s current price, just under $92,000, these bitcoins are worth nearly $6.4 billion, and crypto outlets are reporting that DOJ officials have said they’re planning to proceed with selling off the assets consistent with the court’s order. The DOJ had reportedly argued that bitcoin’s price volatility was a pressing reason to push for permission for the sale.

Ars has reached out to the DOJ for comment and will update the story with any new information regarding next steps.

A hacker initially stole these bitcoins from Silk Road—an illegal online marketplace where goods could only be bought and sold with bitcoins—in 2012, shortly before the US government shut down the marketplace. The US later discovered the stolen bitcoins in 2020 while conducting further investigations of Silk Road, eventually securing a consent agreement that year from the hacker, who signed the bitcoins over to the government.

Whether the government’s seizure of those bitcoins was proper has been disputed by Battle Born Investments, a company that purchased the assets of bankruptcy estate from an individual who they believed to be either the hacker whose bitcoins were seized or someone “associated with him.”

After a court battle failed to return the bitcoins, Battle Born attempted to unmask the hacker through a Freedom of Information Act (FOIA) request, which sparked a new court fight. But ultimately, in late December, the court agreed with the US government that the hacker had a right to privacy as someone who was the subject of a criminal investigation and shouldn’t be unmasked. That ended Battle Born’s claim to the bitcoins and cleared the way for the government’s sale.

But Russia presumably gets no taxes on illegal crypto mining, and power outages can be costly for everyone in a region. So next year, Russia will ban crypto mining in 10 regions for six years and place seasonal restrictions that would disrupt some crypto mining operations during the coldest winter months in regions like Irkutsk, CoinTelegraph reported.

Illegal mining is still reportedly thriving in Irkutsk, though, despite the government’s attempts to shut down secret farms. To deter any illegal crypto mining disrupting power grids last year, authorities seized hundreds of crypto mining rigs in Irkutsk, Crypto News reported.

In July, Russian president Vladimir Putin linked blackouts to illegal crypto mines, warning that crypto mining currently consumes “almost 1.5 percent of Russia’s total electricity consumption,” but “the figure continues to go up,” the Moscow Times reported. And in September, Reuters reported that illegal mines were literally going underground to avoid detection as Russia’s crackdown continues.

Even though illegal mines are seemingly common in parts of Siberia and increasingly operating out of the public eye, finding an illegal mine hidden on state land controlled by an electrical utility was probably surprising to officials.

The power provider was not named in the announcement, and there are several in the region, so it’s not currently clear which one made the controversial decision to lease state land to an illegal mining operation.

Wright’s lawsuit names a defendant he calls “BTC Core,” which apparently doesn’t exist. Wright alleges that BTC Core “partners” include 122 corporate entities and 22 individuals who contributed to bitcoin development and research. Wright also named BTC Core as a defendant in a 2022 lawsuit.

This week’s court ruling said that “COPA (and others) say there is no such entity and it is an invention of Dr. Wright’s in his attempt to designate those who are or who have been involved in the development of the software used in various manifestations of Bitcoin as a partnership. They deny there is any such partnership, as Dr. Wright seems to allege. It is not necessary to resolve that issue.”

Corporations and individuals that Wright claims are part of BTC Core “were defendants to various of the previous actions brought by Dr. Wright (and his companies),” Mellor wrote.

Wright suit “repeat[s] his dishonest claim to be Satoshi”

Wright contended that his lawsuit falls outside the bounds of the previous order because his new claims “do not involve him claiming to be Satoshi Nakamoto and do not depend on him having invented the Bitcoin system,” Mellor wrote. Mellor rejected Wright’s arguments.

For one thing, Mellor said the earlier order “is not limited to prohibiting claims dependent on Dr. Wright asserting that he is Satoshi Nakamoto.” For another, Mellor pointed out that Wright’s latest lawsuit “does include pleaded contentions that he is Satoshi Nakamoto,” and thus “Dr. Wright is wrong to say that his New Claim does not repeat his dishonest claim to be Satoshi.”

Further, COPA contended “that each of the principal claims in the New Claim can only be maintained by Dr. Wright asserting intellectual property rights which the Order precludes him from asserting in legal proceedings.”

Addressing Wright’s copyright claim, Mellor wrote that “Dr. Wright does not claim a license or any assignment from some other person alleged to be owner of copyright in the relevant works. Therefore Dr. Wright cannot bring this claim for copyright infringement without claiming ownership of the rights which he alleges to have been infringed. That is to say, Dr. Wright cannot bring an infringement claim in relation to the works in question, however it is worded, without breaching the Order.”

A bitcoin investor who went to increasingly great lengths to hide $1 million in cryptocurrency gains on his tax returns was sentenced to two years in prison on Thursday.

It seems that not even his most “sophisticated” tactics—including using mixers, managing multiple wallets, and setting up in-person meetings to swap bitcoins for cash—kept the feds from tracing crypto trades that he believed were untraceable.

The Austin, Texas, man, Frank Richard Ahlgren III, started buying up bitcoins in 2011. In 2015, he upped his trading, purchasing approximately 1,366 using Coinbase accounts. He waited until 2017 before cashing in, earning $3.7 million after selling about 640 at a price more than 10 times his initial costs. Celebrating his gains, he bought a house in Utah in 2017, mostly funded by bitcoins he purchased in 2015.

Very quickly, Ahlgren sought to hide these earnings, the Department of Justice said in a press release. Rather than report them on his 2017 tax return, Ahlgren “lied to his accountant by submitting a false summary of his gains and losses from the sale of his bitcoins.” He did this by claiming that the bitcoins he purchased in 2015 were much higher than his actual costs, even being so bold as to claim he as charged prices “greater than the highest price bitcoins sold for in the market prior to the purchase of the Utah house.”

First tax evasion prosecution centered solely on crypto

Ahlgren’s tax evasion only got bolder as the years passed after this first fraud, the DOJ said.

In 2018 and 2019, he sold more bitcoins, earning more than $650,000 and deciding not to report any of it on his tax returns for those years. That meant that he needed to actively conceal the earnings, but he’d been apparently researching how mixers are used to disguise where bitcoins come from since at least 2014, the feds found, referencing a blog he wrote exhibiting his knowledge. And that’s not the only step he took to try to trick the Internal Revenue Service.

Bitcoin hit a new record high late Monday, its value peaking at $89,623 as investors quickly moved to cash in on expectations that Donald Trump will end a White House crackdown that intensified last year on crypto.

While the trading rally has now paused, analysts predict that bitcoin’s value will only continue rising following Trump’s win—perhaps even reaching $100,000 by the end of 2024, CNBC reported.

Bitcoin wasn’t the only winner emerging from the post-election crypto trading. Crypto exchanges like Coinbase also experienced surges in the market, and one of the biggest winners, CNBC reported, was dogecoin, a cryptocurrency linked to Elon Musk, who campaigned for Trump and may join his administration. Dogecoin’s value is up 135 percent since Trump’s win.

On the campaign trail, Trump began wooing the cryptocurrency industry, seeking donations and votes by promising to make the US the “crypto capital of the planet,” Fortune reported. He announced the launch of his own crypto platform, World Liberty Financial (WLFI), and vowed to “fire” Gary Gensler—the Securities and Commission Exchange (SEC) chair leading the US crypto crackdown—on “day one” in office, Al Jazeera reported.

Whether Trump can actually fire Gensler is still up in the air, The Washington Post reported. It seems more likely that Trump may demote Gensler, The Post reported, since people familiar with the matter suggested that “fully outing” the current SEC chair “could trigger a novel and complicated legal battle over the president’s authorities.” So far, Gensler has made no indications that he will step down once Trump takes office, although The Post noted that wouldn’t be considered unusual.

Sources told The Post that Trump is considering “a mix of current regulators, former federal officials, and financial industry executives,” for leadership positions, “many of whom have publicly expressed pro-crypto views.”

Reportedly under consideration to replace Gensler are Daniel Gallagher, a former SEC official currently serving as chief legal officer for the financial technology firm Robinhood, and two Republican SEC commissioners, Hester Peirce and Mark Uyeda, The Post’s sources said. Other names in the mix include a former SEC commissioner, Paul Atkins, and a former commissioner at the Commodity Futures Trading Commission, Chris Giancarlo.

Billy Restey is a digital artist who runs a studio in Seattle. But after hours, he hunts for rare chunks of bitcoin. He does it for the thrill. “It’s like collecting Magic: The Gathering or Pokémon cards,” says Restey. “It’s that excitement of, like, what if I catch something rare?”

In the same way a dollar is made up of 100 cents, one bitcoin is composed of 100 million satoshis—or sats, for short. But not all sats are made equal. Those produced in the year bitcoin was created are considered vintage, like a fine wine. Other coveted sats were part of transactions made by bitcoin’s inventor. Some correspond with a particular transaction milestone. These and various other properties make some sats more scarce than others—and therefore more valuable. The very rarest can sell for tens of millions of times their face value; in April, a single sat, normally worth $0.0006, sold for $2.1 million.

Restey is part of a small, tight-knit band of hunters trying to root out these rare sats, which are scattered across the bitcoin network. They do this by depositing batches of bitcoin with a crypto exchange, then withdrawing the same amount—a little like depositing cash with a bank teller and immediately taking it out again from the ATM outside. The coins they receive in return are not the same they deposited, giving them a fresh stash through which to sift. They rinse and repeat.

In April 2023, when Restey started out, he was one of the only people hunting for rare sats—and the process was entirely manual. But now, he uses third-party software to automatically filter through and separate out any precious sats, which he can usually sell for around $80. “I’ve sifted through around 230,000 bitcoin at this point,” he says.

Restey has unearthed thousands of uncommon sats to date, selling only enough to cover the transaction fees and turn a small profit—and collecting the rest himself. But the window of opportunity is closing. The number of rare sats yet to be discovered is steadily shrinking and, as large organizations cotton on, individual hunters risk getting squeezed out. “For a lot of people, it doesn’t make [economic] sense anymore,” says Restey. “But I’m still sat hunting.”

Rarity out of thin air

Bitcoin has been around for 15 years, but rare sats have existed for barely more than 15 months. In January 2023, computer scientist Casey Rodarmor released the Ordinals protocol, which sits as a veneer over the top of the bitcoin network. His aim was to bring a bitcoin equivalent to non-fungible tokens (NFTs) to the network, whereby ownership of a piece of digital media is represented by a sat. He called them “inscriptions.”

There had previously been no way to tell one sat from another. To remedy the problem, Rodarmor coded a method into the Ordinals protocol for differentiating between sats for the first time, by ordering them by number from oldest to newest. Thus, as a side effect of an apparatus designed for something else entirely, rare sats were born.

By allowing sats to be sequenced and tracked, Rodarmor had changed a system in which every bitcoin was freely interchangeable into one in which not all units of bitcoin are equal. He had created rarity out of thin air. “It’s an optional, sort of pretend lens through which to view bitcoin,” says Rodarmor. “It creates value out of nothing.”

When the Ordinals system was first released, it divided bitcoiners. Inscriptions were a near-instant hit, but some felt they were a bastardization of bitcoin’s true purpose—as a system for peer-to-peer payments—or had a “reflexive allergic reaction,” says Rodarmor, to anything that so much as resembled an NFT. The enthusiasm for inscriptions resulted in network congestion as people began to experiment with the new functionality, thus driving transaction fees to a two-year high and adding fuel to an already-fiery debate. One bitcoin developer called for inscriptions to be banned. Those that trade in rare sats have come under attack, too, says Danny Diekroeger, another sat hunter. “Bitcoin maximalists hate this stuff—and they hate me,” he says.

The fuss around the Ordinals system has by now mostly died down, says Rodarmor, but a “loud minority” on X is still “infuriated” by the invention. “I wish hardcore bitcoiners understood that people are going to do things with bitcoin that they think are stupid—and that’s okay,” says Rodarmor. “Just, like, get over it.”

The hunt for rare sats, itself an eccentric mutation of the bitcoin system, falls into that bracket. “It’s highly wacky,” says Rodarmor.

{kind=link}