I obviously cover many economical things in the ordinary course of business, but I try to reserve the sufficiently out of place or in the weeds stuff that is not time sensitive for updates like this one.

Alex Recouso: The recent capital gains tax increase in the UK was expected to bring additional tax revenue.

Instead, high-net-worth individuals and families are leaving the country leading to an 18% fall in net capital gains tax revenue. A £2.7b loss.

Welcome to the Laffer curve, suckers.

Here’s what looks at first like a wild paper, claiming that surge pricing is great overall and fantastic for riders increasing their surplus by 3.57%, but that it decreases driver surplus by 0.98% and the platform’s current profits by 0.5% of gross revenue.

At first that made no sense, obviously raising prices will be good for drivers, and Uber wouldn’t do it if it lowered revenue.

This result only makes sense once you realize that the paper is not holding non-surge pricing constant. It assumes without surge pricing, Uber would raise their baseline rates substantially. That’s also why this is bad for workers with long hours at off-peak times, as their revenue declines. Uber could raise more revenue now with higher off-peak hours, but it prefers to focus on the long term, which helps riders and hurts drivers.

That makes sense, but it also raises the question of why Uber is keeping prices so low at this point. Early on, sure, you’re growing the market and fighting for market share. But now, the market is mature, and has settled into a duopoly. Is Uber that afraid of competition? Is it simply corporate culture and inertia? I mean, Uber, never change (in this particular way), but it doesn’t seem optimal from your perspective.

Story mostly checks out in theory, as the practice is commonly used, with some notes. If tips are 90%+ a function of how much you tip in general, and vary almost none based on service, at equilibrium they’re mostly a tax on tippers paid to non-tippers.

Gabriel: it’s actually hilarious how tipping is just redistribution of capital from people pleasers to non people pleasers

tipping never increases salaries in the long run because free markets, so our entire tip becomes savings of the rude people that don’t tip ironically.

say waiters started earning 30% more from tips, then everyone wants to become a waiter, and now businesses can decrease salaries to match market value. more restaurants will be started from tipping, not an increase in salary

tipping would have served a great purpose if it was socially acceptable to not tip, cause people doing a great job and who are nice would be paid more than the not nice people

i always tip cause i feel bad if i wouldn’t, but in theory your tip makes no difference and markets would adjust accordingly in the long run (but slightly inefficiently since you’d be spending less until menu prices actually increase)

Nitish Panesar: It’s wild how “voluntary” generosity just ends up subsidizing the less generous Makes you wonder if the system is rewarding the exact opposite of what we hope.

It’s not only a distribution from pleasers to non-pleasers, it is also from truth tellers to liars, because being able to say that you tip, and tip generously, is a lot of what people are really buying via their tips.

There are some additional effects.

The menu price illusion effect raises willingness to pay, people are silly.

Tax policy (e.g. ‘no tax on tips’ or not enforcing one) can be impacted.

Tips can create an effective floor on server pay if a place has some mix of high prices and general good tippers, assuming the tips don’t get confiscated. That floor could easily bind.

If you tip generously as a regular, some places do give you better service in various ways that can be worthwhile. And if you tip zero or very low systematically enough that people remember this, there will be a response in the other direction.

Note that the network of at least the Resy-level high end restaurants keep and share notes on their customers. So if you tip well or poorly at that level, word will likely get out, even if you go to different places.

It is also likely that you can effectively do acausal trade a la Parfit’s Hitchhiker (Parfit’s Diner?) as I bet waiters are mostly pretty good at figuring out who is and is not going to tip well.

The other factor is, even if tipping as currently implemented doesn’t work in theory, it seems suspiciously like it works in practice – in the sense that American service in restaurants in particular is in general vastly better than in other places. It’s not obvious whether that would have been true anyway, but if it works, even if it in theory shouldn’t? Then it is totally worth all the weird effects.

The tax benefits of rewarding people via orgies, as a form of non-wage compensation. That is on top of the other benefits, as certain things cannot be purchased, purchased on behalf of others or even asked for without degrading their value. The perfect gift!

Noah Smith explains that the divergence between mean productivity and median wages is mostly about unequal compensation, and when you adjust the classic divergence chart in several ways, the gap between wages and productivity declines dramatically, although not entirely:

That also says that real median wages are up 16.3% over that period. One can also consider that this is all part of the story of being forced to purchase more and better goods and services, without getting the additional funds to do that. As I’ve said, I do think that life as the median worker did get net harder over that period, but things are a lot less crazy than people think.

For starters, what the hell does that actually mean? When advocates cite it, they clearly mean that such people are ‘one expense away from disaster’ but the studies they cite mostly mean something else, which is a low savings rate.

It seems all the major surveys people cite are actually asking about low savings rate.

The go-to LendingClub claim that it’s 60% of Americans asks if someone’s savings rate is zero or less. We also have BankRate at 34%, asking essentially the same question, that’s a huge gap. Bank of America got 50% to either agree or strongly agree.

Bank of America also looked at people’s expenses in detail to see who used 95% or more of household income on ‘necessity spending’ and got 26% but that whole process seems super weird and wonky, I wouldn’t rely on it for anything.

Whereas the median American net worth is $192,700 with a liquid net worth of $7,850. Which after adjustments is arguably only a month of income. But 54% of Americans, when asked in a survey, said they had 3 months of savings available. But then 24% of people who said that then said they ‘couldn’t afford’ an emergency expense of $2k, what? So it’s weird. $8k is still very different from the ‘most Americans can’t pay a few thousand in expenses’ claims we often see, and this is before you start using credit cards or other forms of credit.

So, yeah, it’s all very weird. People aren’t answering in ways that are logically consistent or that make much sense.

What is clear is that when people cite how many Americans are ‘living paycheck to paycheck,’ almost always they are presenting a highly false impression. The map you would take away from that claim does not match the territory.

In addition to the ‘half of Americans live paycheck to paycheck’ claims being well-known to be objectively false, there’s another mystery behind them that Matt Yglesias points out. What policies would prevent this from being true? The more of a social safety net you provide, the less costly it is to live ‘paycheck to paycheck’ and the more people will do it. If you want people to have savings that aren’t in effect provided by their safety nets, then take away their safety net, watch what happens.

Unrealized capital gains create strange incentives. How much do the rich practice ‘buy, borrow, die’? The answer is some, but not all that much, with such borrowing being on average only 1-2% of economic income. Mostly they ‘buy, save, die,’ as their liquid incomes usually exceed consumption. The loophole should still be closed, especially as other changes could cause it to matter far more, but what matters is the cost basis step-up on death. There should at minimum be a cap on that.

Patrick McKenzie goes insanely deep on the seemingly unbelievable story about a woman withdrawing $50k in cash at the bank with very little questioning, and then losing it to a scammer. After an absurd amount of investigation, including tracking down The Room Where It Happened, it turned out the story all made sense. The bank let her withdraw the money because, if you take into account the equity in her house, she was actually wealthy, and the bank knew that so $50k did not raise so many alarm bells.

Patrick McKenzie pushes back against the idea that interchange fees and credit card rewards, taken together, are regressive redistribution. I find his argument convincing.

Refund bonuses on crowdsourced projects give good incentives and signals all around, so they are highly effective at attracting more funding for privately created public goods. The problem is that if you do fail to fund or fail to deliver, and need to give out the bonus, that is a rather big disaster. So you win big on one level, and lose big on another. If I’m actively poorer when I fail, I’m going to have a high threshold for starting. Good selection, but you lose a lot of projects, some of which you want.

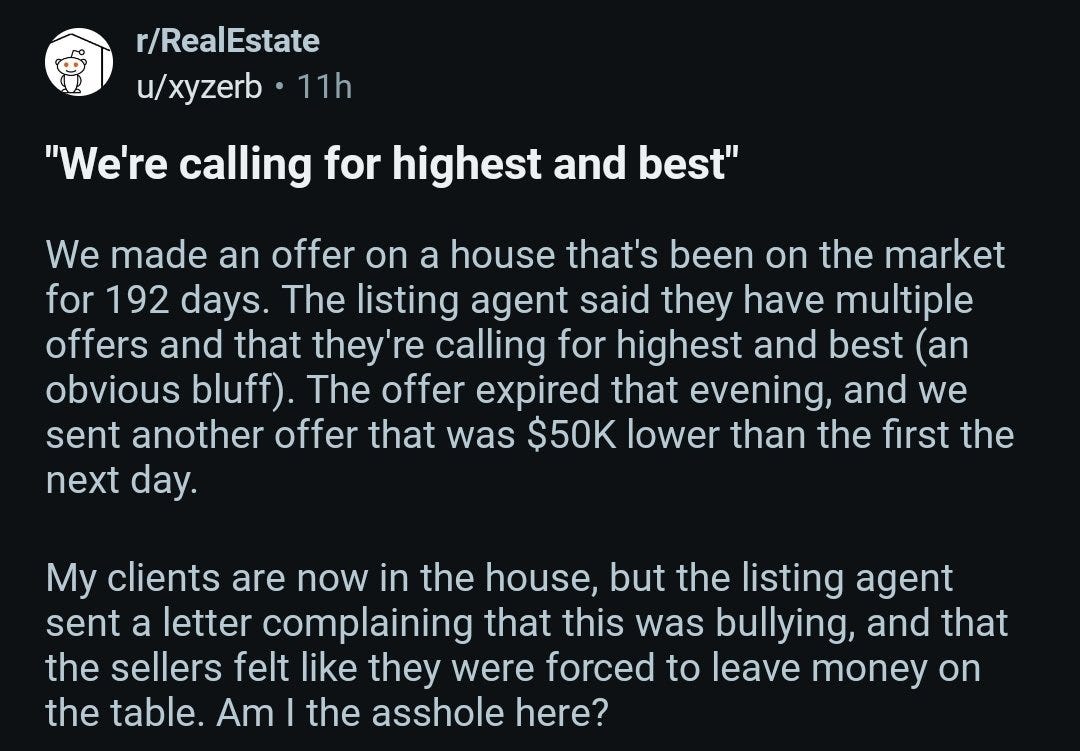

Austen Allred: I just realized the buyer’s agent in a real estate transaction has no incentive to help their customers get a better price

“But the agent isn’t going to rip you off, if you save $50k they only lose $1500.”

They’re just not going to scratch and claw to save every penny the same way I would if it were my money. Example: Very easy to say, “It’s competitive you should just put an offer in at asking.”

“But they want referrals.” Sure, but they have all of the information about what is reasonable and not.

“But they have a code of ethics.” Lol. Lmfao.

Given the math it’s very obvious that it’s a volume game. A real estate agent gets paid not by saving or making money, but by pushing deals through. It’s very clear incentive misalignment.

How does a buyer know if a deal is competitive, or if they need to move quickly? If the buying agent tells them it is. How does the buying agent know if a deal is competitive? If the selling agent tells them so. I’m sure that’s never been abused ever.

Steven Sinofsky: Anyone who has ever bought or sold a house comes to realize you’re mostly negotiating with your own agent, while your agent is mostly colluding with the other agent against both buyer and seller offering back incomplete information—an entirely unaligned transaction experience.

Sam Pullara: it is extremely difficult to align agents

Austen Allred: OpenAI has a team for that.

Astrus Dastan: And they’re failing miserably.

Yep, if you get 3% of the sale price you’re not going to fight for the lowest (or even highest, for the seller, if it means risking or dragging out the sale) possible price on that basis. It’s a volume business. But also it’s a reputation and networking business.

What this is missing is that I got my real estate agent because my best friend referred her to me, and then she actively warned us off of buying a few places until we found the right one and walked me through all the steps, and then because she did a great job fighting for me I recommended her to other clients and she got two additional commissions. The incentives are there.

As for the quoted transaction, well, yes, they were forced to leave money on the table because their agent negotiated with a dishonest and risky strategy, got their bluff called and it backfired. Tough. I’m guessing there won’t be a recommendation there.

People also think businesses try to follow the Ferengi Rules of Acquisition, basically?

Rashida Tlaib: Families are struggling to put food on the table. I sent a letter to @Kroger about their decision to roll out surge pricing using facial recognition technology. Facial recognition technology is often discriminatory and shouldn’t be used in grocery stores to price gouge residents.

Leon: >walk into kroger with diarrhea

>try to make my face seem normal

>grab $5 diarrhea medicine

>sharp pain hits my gut

>diarrhea medicine now costs $100

Something tells me that if they do that, then next time, if you have any choice whatsoever (and usually you do have such a choice) you’re not going to Kroger, and that’s the best case scenario for your reaction here. That’s the whole point of competition and capitalism.

What would actually happen if Kroger had the ability to do perfect price discrimination based on facial recognition? Basic economics says there would be higher volumes and less deadweight loss. Assuming there was competition from other stores such that profits stayed roughly the same, consumers would massively benefit.

The actual danger is the ‘try to make my face seem normal’ step. If you can plausibly spend resources to fool the system, then that spends everyone’s time and effort on games that do not produce anything. That’s the part to avoid. We’ve been doing this for a long time, with coupons and sales and other gimmicks that do price discrimination largely on the basis of willingness to do extra work. If anything basing on facial recognition seems better at that, and dynamic pricing should be better at managing inventory as well.

Dwarkesh Patel: I asked Victor Shih this question – why has the Chinese stock market been flat for so long despite the economy growing so fast?

This puzzle is explained via China’s system of financial repression.

If you save money in China, banks are not giving you the true competitive interest rate. Rather, they’ll give you the government capped 1.3% (lower than inflation, meaning you’re earning a negative return).

The net interest (which is basically a tax on all Chinese savers) is shoveled into politically favored state owned enterprises that survive only on subsidized credit.

But here’s what I didn’t understand at first: Why don’t companies just raise equity capital and operate profitably for shareholders?

The answer apparently is that there’s no ‘outside’ the system.

The state doesn’t just control credit – it controls land, permits, market access, even board seats through Party committees. Companies that prioritize profits over market share lose these privileges. Those that play along get subsidized loans, regulatory favors, and government contracts.

Regular savers, founders, and investors are all turned into unwitting servants of China’s industrial policy.

The obvious follow-up question is why is there not epic capital flight by every dollar that isn’t under capital controls? Who would ever invest in a Chinese company if they had a choice (other than me, a fool whose portfolio includes IEMG)? Certainly not anyone outside China, and those inside China would only do it if they couldn’t buy outside assets, even treasuries or outside savings accounts. No reason to stick around while they drink your milkshake.

This falls under the category of ‘things that if America contemplated doing even 10% of what China does, various people would say this will instantly cause us to ‘Lose to China’’. I very much have zero desire to do this one, but perhaps saying that phrase a lot should be a hint that something else is going on?

It’s also fun to see the cope, that this must be all that free market competition.

Amjad Msad: This doesn’t make much sense. China’s market is hyper competitive. In other words, it’s the opposite of socialist. That’s why you see thinner margins and more overall dynamism than US markets.

Yes, it’s hyper competitive, and the ways in which it is not socialist are vital to its ability to function, but that hyper competition is, as I understand it, ‘not natural,’ and very much not due to the invisible hand, but rather a different highly visible one.

We couldn’t pull it off and shouldn’t try. The PCR’s strategy is a package deal, the same way America’s strategy is a package deal, and our strategy has been the most successful in world history until and except where we started shooting ourselves in the foot. They are using their advantages and we must use ours. If we try to play by their rules, especially on top of our rules, they will win.

John Arnold: CA raised min wage for fast food workers 25% ($16 -> $20) and employment in the sector fell 3.2% in the first year. While I hate sectoral specific min wage laws, this is less than I’d have thought. That said, the real risk is tech substitutes for labor over long term, not year 1.

Claude estimates 70% of employees were previously near minimum wage and only maybe 10% were previously over $20. It estimates the average wage shock at around 14%, although this is probably an underestimate due to spillover effects (as in, you have to adjust higher wages so that rank orders are preserved). If this was a more than 14% raise and employment only fell 3.2%, then on its face that is a huge win.

You then have to account for effects on things like hours, overtime and other work conditions, and for long term effects being larger than short term effects, since a lot of investments are locked in and adjustments take time. But I do think that this is a win for ‘minimum wage increases are not as bad for employment as one would naively think and can be welfare enhancing for the workers,’ of course it makes things worse for employers and customers.

A new report from the Ludwig Institute for Shared Economic Prosperity (uh huh) claims 60% of Americans cannot afford a ‘minimal quality of life.’

This is the correct reaction:

Zac Hill: This is just obviously false, though.

Daniel Eth: Okay, so… this “analysis” is obvious bullshit.

I mean, obviously. Are you saying the median American household can’t afford a ‘minimal quality of life’? That’s Obvious Nonsense. Here’s a few more details, I guess:

Megan Cerullo (CBS): LISEP tracks costs associated with what the research firm calls a “basket of American dream essentials.”

…

The Ludwig Institute also says that the nation’s official unemployment rate of 4.2% greatly understates the level of economic distress around the U.S. Factoring in workers who are stuck in poverty-wage jobs and people who are unable to find full-time employment, the U.S. jobless rate now tops 24%, according to LISEP, which defines these groups as “functionally unemployed.”

Claiming the ‘real unemployment rate’ is 24% is kind of a giveaway. So is saying that your ‘minimal quality of life’ costs $120,302 for a family of four, sorry what in hell? Looking at their methodology table of contents tells you a lot about what are they even measuring.

Luca Dellanna: The study considered necessary for “Minimal Quality of Life”, I kid you not, attendance of two MLB games per year per person.

Do these charlatans hope no one reads their studies?

That’s not quite fair, the MLB games and six movies a year are a proxy for ‘basic leisure,’ but that kind of thing is happening throughout.

I love this: Businesses ‘setting traps’ for private equity by taking down their website, so Private Equity Guy says ‘oh I can get a big win by giving them a website’ and purchases your business, but the benefits of your (previously real) website are already priced in. You don’t even have to fool them, they’ll fool themselves for you:

Lauren Balik: One of the biggest hacks for small business owners is removing your website in order to sell your company at a premium.

For example, I used to have a website, then I took it down and all of a sudden I was getting legitimate, fat offers to buy my business.

See, private equity people are lazy as hell. They get data from databases showing revenue proxies, run rate estimates, all kinds of ZoomInfo crap, etc. and they are willing to pay large premiums for easy, quick wins.

What’s the easiest, quickest win? Making a website for a business that has no website.

“Wow, this business is doing $1.5M a year and $500k EBITDA with no website. Imagine if we made a website! We could get this to $3M gross and $1.5M EBITDA overnight!”

Because private equity people are narcissistic, they don’t even consider that a small business owner may have outfoxed them and purposely taken down their website to set a trap.

You should be doing less, not more, and baiting snares for PE.

Hunter: Maybe a few fake bad reviews about the owners aren’t properly leveraging technology.

Mark Le Dain (from another thread): If you are planning to sell a plumbing company to PE make sure you get rid of the website before selling it They love to say “and I can’t even imagine what it will be like once we add a website and a CRM”

Lauren Balik: It even happens at scale. Subway pulled this on Roark lmfao.

People think I make stuff up. All throughout late 2023 and early 2024 Subway started breaking their own website and making it unusable for customers as Subway was trying to put pressure on Ayn Rand-inspired PE firm Roark Capital to close the acquisition.

Every time the website lost sales or went down it put more pressure on Roark to close the deal, which was finally completed in April 2024.

Should GDP include defense spending? The argument is it is there to enable other goods and services, it is not useful per se. To which I say, tons of other production is also there to enable other goods and services. Even if we’re talking purely about physical security, should we not count locksmiths or smoke alarms or firefighting? Should we not count bike helmets? Should we not count advertising? Should we not count goods that are not useful, or are positional or zero-sum? Lawyers? Accountants? All investments? Come on.

It is fine to say ‘there is a measure of non-defense production and it is more meaningful as a measure of living standards,’ sure, but that is not GDP. But if we are measuring living standards, a much bigger issue is that cost is very different from consumer surplus, especially regarding the internet and soon also AI.

Roon notices that as Taleb told us there is almost never a shortage that is not followed by a glut, and wonders why we ever need to panic about lack of domestic production if others want to subsidize our consumption. The answer is mostly mumble mumble politics, of course, except for certain strategically vital things we might lose access to (e.g. semiconductors) or where it’s the government that’s stopping us from producing.

While we wait for the verdict on Anthropic’s Claude Sonnet 3.7, today seems like a good day to catch up on the queue and look at various economics-related things.

No tax on tips. It’s dumb, but it’s a campaign promise. He notes that as long as people still have to declare their tips, and we don’t allow those with high incomes to pretend to take half their income in tips, not taxing tips directly won’t matter much, so we should relax.

I think this is far too big an assumption of competence, but given this has to get through Congress, we’re probably safe from the madness.

No tax on social security. He explains why the benefits shouldn’t be taxed.

I get that, but this is a big benefits increase, in a way that doesn’t seem necessary, that transfers money from young to elderly, and which puts a lie to every other ‘we are running out of money’ complaint.

No tax on overtime pay. This one is sufficiently stupid that he can’t pretend that it would not be a huge disaster, the incentives are so awful.

Renewing the Trump tax cuts. Yeah, yeah. Probably a good idea.

Adjusting the SALT cap. He’s against this because of the incentive it gives to states to raise their income taxes.

I notice that when SALT was capped no states lowered their income taxes? He’s only going to fiddle at margins anyway.

Closing the carried interest “loophole.” He says this one is unclear. He points out actual capital gains taxes are stupid, so we should be thankful the rate on those is lower (true), and given this is the case the financial wizards would only find a new loophole.

The level of friction required to get loopholes matters, and indeed many out there already do actually pay their taxes, myself included.

Most of this tax break is going to hedge funds and private equity, I don’t see any reason the tax code should be encouraging these forms of business. I’m not against them, but we are likely allocating too much capital and talent here.

A small portion of the tax break goes to venture capitalists, and yes this part is good policy and we should try to preserve that part of it or make up for it some other way.

Norway doubles down on its unrealized capital gains tax strategy, including an exit tax of 38% of net assets including unrealized gains, despite having a gigantic sovereign wealth fund from its oil wealth. Norway has a lot of ruin in it due to the oil and high human capital, but this is painful to see.

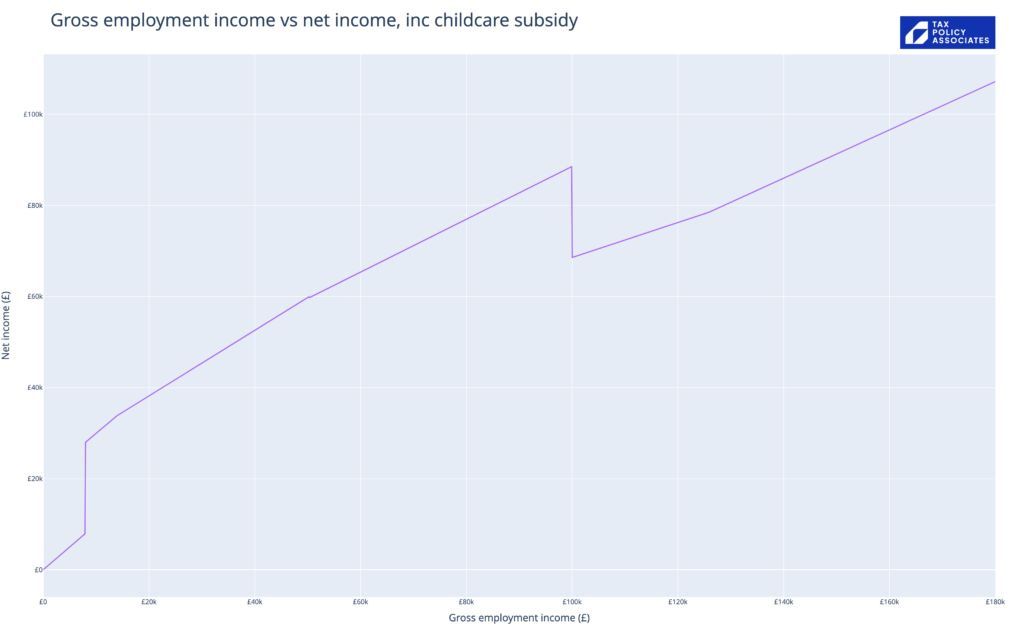

Dan Neidle: The 20,000% spike at £100,000 is absolutely not a joke – someone earning £99,999.99 with two children under three in London will lose an immediate £20k if they earn a penny more. The practical effect is clearer if we plot gross vs net income:

David Algonquin: This must be one of the worst pieces of tax policy design ever. I know people who have dropped down to a 4-day week or, if self-employed, take on less work to avoid this trap.

That’s hard to see, but it means that in this scenario you are better off making 99k than 100k+, unless you can make over ~145k. Normally it’s nowhere near this crazy, but you can be a lot less crazy than this and still rather crazy.

Dan Neidle: It’s perfectly coherent and rational to think high earners should pay 62% tax (and of course also coherent and rational to disagree).

But surely nobody thinks we should have 62% tax on people earning £100k-125k, and 47% on people earning more than £125k?

And it can get worse. If Jane’s still repaying her student loan, that’s another 9% – the student loan system behaves like a crude graduate tax. Jane’s marginal rate reaches 71%.

Europe still has sufficiently strong trade barriers that they are equivalent to a 45% tariff on manufacturing and 110% for services, according to Mario Draghi. That’s without even considering the ‘trade barriers’ that exist within-countries in the form of ‘EU being the EU.’ o3-mini-high estimated that this costs the EU RGDP growth in the range 0.2%-0.5% per year, versus taking those barriers down.

A similar situation exists between Canadian provinces, which continues to blow my mind because not only is it a huge own goal for no reason, it is so profoundly unpopular and everyone wants to get rid of it, and somehow it is still there.

One serious danger with the new administration is a potential cap on credit card interest rates at 10%, with Senators Sanders and Hawley planning to work on this with President Trump. This would severely limit the ability of the poor, or those with poor credit, to access credit cards, and the alternatives to credit cards are all vastly worse.

We also had yet another round of people falsely claiming that 60% of Americans live paycheck to paycheck, for various reasons this claim simply will not die despite a majority of Americans having actual cash savings that can pay for 3 months of expenses, even before dipping into credit cards, and the median household having a net worth of $193k. There are horrible crimes of statistics happening around such claims, in both directions, but the central truth is very clear.

Damon Chen: My friend told me he and his wife live paycheck to paycheck.

I don’t believe it because they both are high earners in tech, and he even works for Google. But after doing a little bit of math, I found out he didn’t lie.

• Mortgage: $17,000/month for a $3M home

• Property Tax: $3,000/month

• Private School: $3,000/month for 1 kid

• Travel: $2,000/month (assuming $20k/year)

• Utilities: $1,000/month

• Groceries: $2,000/month

• Eating Out: $1,000/month

• 2 cars: $1,000/month

So in total $30k per month, not including other misc costs like house maintenance, paying for Netflix, etc.

W-2 employees usually take home only 50% of their salary, so they have to make $60k per month pretax, which is $720k in annual TC.

What’s the point of living a life like this?

This is almost entirely housing and taxes. They’re paying California taxes, which is an extra 10% or so of gross income in this income range, or about $6k/month at $720k annual, and the property costs $21k including utilities (which seem strangely high for a region without much need for heat or AC, are they doing a ton of EV charging maybe? If so that half of it should be filed under the cars). That’s $27k, everything else costs a combined $9k.

Cutting other spending won’t make that much difference for them. Yes, $20k/year for travel (that can’t be expensed) seems crazy to me, but some people value it. Others are saying groceries and eating out are too high here, again there is room to cut but I do think you can get a lot of value from the premium there. So it really does come down to, how much does a family of three want a $3 million home (with a not fun interest rate)?

I’d also question buying both a $3 million home and a private school. If you’re paying that much, presumably (since he’s working at Google) they’re in Palo Alto, which does kind of justify the home price if you want to go large enough to plan for a big family, but then that area is said to have excellent public schools. It’s a hell of a lot to pay for that shorter commute.

Presumably this is because the franchise value and forward deal flow of VC firms was cratered so much by government crackdowns that the firms have chosen to hound past founders despite knowing this destroys their future deal flow. All that’s left is to get what they can from their existing obligations, which in China technically gave them the opportunity to do this, and now they’re actually doing it at scale.

One assumes that no sane person would sign such terms now that the equilibrium has shifted. It’s one thing to have confidence in your startup and take a shot knowing the odds are against you. It’s another thing to do that when failure ruins your life.

From most perspectives I know, this makes absolutely no sense. It is the ultimate ‘isn’t there someone you forgot to ask’ meme. It’s not even a reduction to what the judge considered reasonable, it’s throwing out the entire package.

Paul Graham: It used to be automatic for startups to incorporate in Delaware. That will stop being the case if activist judges start overruling shareholders.

This evening the CEO of a public company told me that all startups should reincorporate in Nevada. That’s apparently the best alternative, and for startups that are still private it’s trivially easy.

The judge’s explanations are, again by most perspectives I know, absurd.

Judge McCormick: Even if a stockholder vote could have a ratifying effect, it could not do so here. Were the court to condone the practice of allowing defeated parties to create new facts for the purpose of revising judgments, lawsuits would become interminable.

“We can’t allow defeated parties to create new facts”? What the actual ? I mean, do you even hear yourself? This makes no sense.

Similarly, claims that the disclosures on the current round were not good enough? They literally stapled the judge’s previous ruling to the disclosures, and were very very clear what Musk was getting, even though it was now vastly more valuable. Absurd.

I presume Judge McCormick’s actual logic is something else entirely. I presume it is some combination of:

Elon Musk broke the rules, and potentially committed outright fraud, by using a compliant board to give him an absurd pay package. We cannot allow him to use this to create an anchor from which he will then benefit.

I don’t think it’s reasonable to pay this much money, and I have the right to impose that opinion on Tesla.

Seriously, though, fthis guy.

Should startups respond to this by reincorporating in Nevada? I have not done the research on the host of other consequences, but my assumption would be no. This is an extraordinary case that is unlikely to be a meaningful precedent. Most of the time, when someone has the level of chutzpah and obviously unacceptable self-dealing that Musk has, invalidating their absurdly huge pay package is a reasonable decision. I see why people would be concerned, but I see this as a one off.

I also see this as part of the standard warning from the startup and Paul Graham crowd, or the Marc Andreessen crowd, that if anyone ever does something they don’t like, that entity will rue the day, rue the day I tell you, because either the startup ecosystem will be Ruined Forever or everyone involved will pick up their balls and go elsewhere. The sky is always about to be falling. Usually, the sky is fine.

I mean, obviously, if you had a full time machine. The sky’s the limit, then. But what if you only had a glimpse to work with and limited options?

In the ‘Crystal Ball Trading Game’ players are given $1 million in play money, and 15 opportunities to see the front page from two days in the future (on the same 15 randomly chosen days) and then trade, with up to 50 times leverage, the S&P 500 and 30-Year Treasuries, evaluated at tomorrow’s close. They report that the median trader, from a mostly savvy pool, had only $687,986 left.

Spencer Jakab: But how does one explain the median loss of 31%? Surely being able to bet heavily on the really obvious, no-brainer newspaper headlines should make up for a few errors? In fact that proved to be many players’ financial undoing, with a not-insignificant number having negative money by the end. The first lesson from the game, then, might be to curb your enthusiasm in such cases.

Any true inhabitant of The River would think very differently about this.

You are being given a one-time unique opportunity. There are no transaction or financing costs, so you definitely have an edge however small, but you only get 15 moves, some with clearer edge than others. The more money you make early, the more you can bet later.

Yes, there are decreasing marginal returns to money, but you’re not in that much danger of hitting them. If you bet at random with the maximum 50x leverage on the S&P for 15 random uncorrelated days, you probably don’t even go broke.

So in that situation, you would correctly want to risk ‘going broke’ within the experiment, bet with giant leverage, and act such that, unless you are outstandingly good at directional predictions, more often than not you lose money.

This contrasts with the story of giving someone 30 minutes of 60/40 coin flips and $25 to bet, with a maximum win of $250. If you can’t win the max almost all the time there, you’re doing something very wrong. Indeed, you should play remarkably conservatively, exactly because you should have no trouble hitting the cap. So instead of betting Kelly’s 20% each time, you should bet substantially less than that.

However, suppose the experiment was very different and you didn’t have a $250 limit. But again, you only have 30 minutes. So you get a 60/40 flip as fast as you can name the sizing and do the flip. Let’s say you can, if you do your sizing quickly, do 4 flips a minute, so you get 120 flips. Kelly only wins you a few thousand dollars on average. If you instead bet half each time, you average a few million. You should definitely be at least that aggressive here given the time limit, at least until you get quite a lot of funds in hand.

Remember Ocean’s 11. The house always wins, unless when you have the edge, you bet big, and then you take the house.

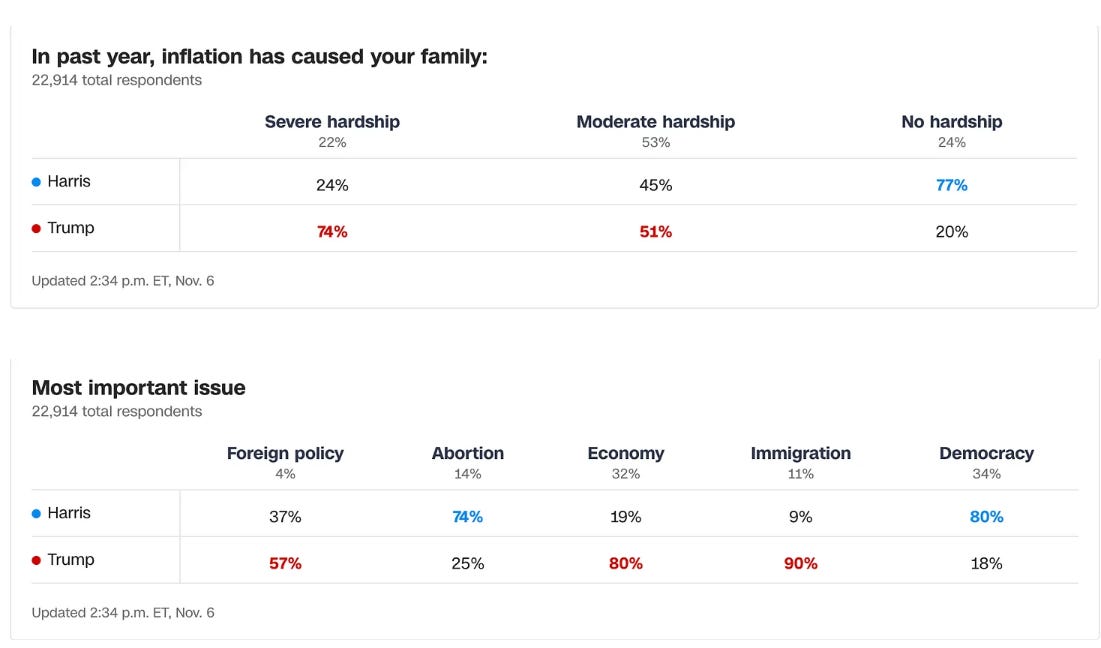

This data very clearly says that people’s economic perceptions are being heavily warped by that hell of a drug, partisanship, in both directions. There’s no other way this data makes sense. What are people thinking?

Zachary Mazlish: Well, turns out, if you are so bold as to close FRED for a second and ask people, 81% of people believe that prices increase faster than wages during inflationary times, and 73% of people believe their purchasing power decreases.

But are they right?

…

I myself have been extremely confused about this issue, and after having spent the bulk of my post-election haze trying to decipher things, I can now report in high spirits that I am only somewhat confused.

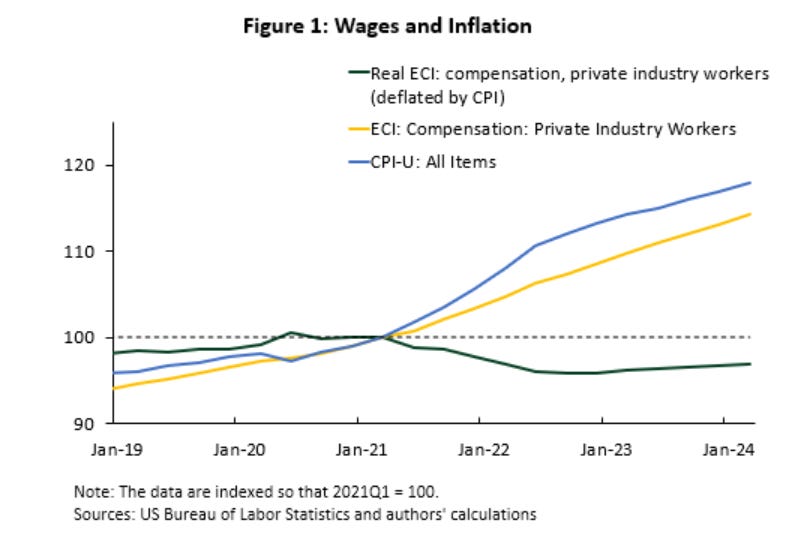

Inflation did make the median voter poorer during Biden’s term.

In no part of the income distribution did wages grow faster while Biden was President than they did 2012-2020.

This is true in the raw data, and even more stark after compositional adjustment.

In particular, the change in median incomes was well below its 2012-20 run-rate.

But, the change in median wages is not what matters; it is the median change in wages that does. And this metric was even weaker under Biden: lower than any period in the last 30 years other than the Great Recession.

People do not feel wages, they feel total income. And median growth in total income — post taxes and transfers — was not just historically low: it collapsed and was deeply negative from 2021 onwards.

Much of this decline is due to timing of pandemic stimulus and even less the “fault of Biden” than other things.

So on #1, the obvious response is, that wasn’t the question. That does not tell you whether people were made poorer, it tells you they became overall less richer. But that’s fine, this was only the setup.

Why is this what matters? It’s a bizarre metric. Why should we care what the median change was, instead of some form of mean change, or change in the mean or median wage? Unless the claim is that voter perception is shaped primarily by their own change in income. That could be a political story but it isn’t a story about economic reality.

So we’re saying that what is happening here is that voters are evaluating income post taxes and transfers, purely for themselves, and then blaming the result on inflation? Perhaps they are indeed doing that, and you can’t do that. I mean, obviously you can, but it’s not a map that matches the territory, again unless the territory you care about is perception.

The attempt to justify #2 is… not great:

To see why the median change in wages is the relevant object for thinking about the election, imagine a world where you had 3 different people: person A with an income of $4, person B with an income of $5, and person C with an income of $10. If four years later person A is now only making $1, person B is making $6, and person C is also making $6, the median income has increased!

But if there were an election, the median worker — who is also the median voter2 —did not have a good last four years, financially speaking. Hence why the median change in income is the object of interest.

In this world, mean income went from $6.66 to $4.33. Of course everyone thinks things got a lot worse. The median income happened to go up, but wages overall are dramatically down. It’s a perverse example, where median income happens to be horribly misleading.

Contrast that with this world (all numbers in real terms):

Time period 1: A makes $1, B makes $6, C makes $10.

Time period 2: A makes $10, B makes $5, C makes $9.

The median change in income is negative, two out of three people saw their wages decline. Do you think this means the economy got worse?

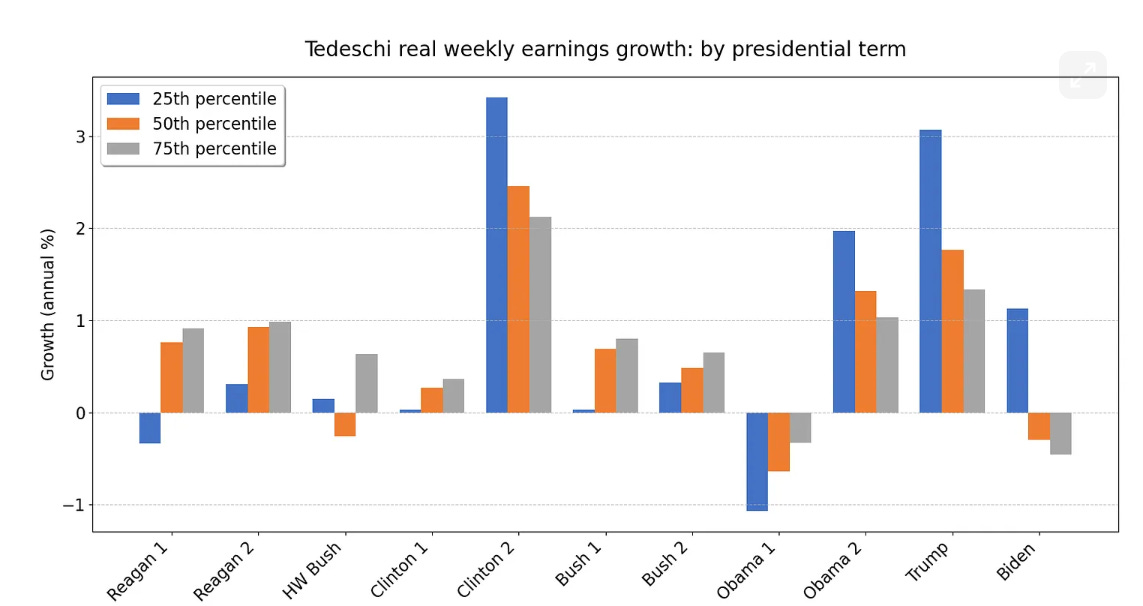

Here’s another graph.

That does look like poor (although still net slightly positive) performance for Biden.

In my opinion, weekly earnings are more relevant than hourly earnings for understanding voter psychology, and likewise, annual earnings are more relevant than weekly earnings: it is annual earnings that determines the overall state of your finances.

This seems to me like a well researched story about voter psychology, that is then being portrayed as inflation making people actually poorer, when we can’t even attribute the voter psychological reaction to the inflation, without knowing the counterfactual.

And indeed, the third point makes clear a lot of what this was about:

Point 3: Post all taxes and transfers, the median household’s real income collapsed while Biden was in office — due to the timing of the Pandemic stimulus.

Yes, exactly. The story is that the big subsidies happened under Trump, and then got taken away, and voters blamed Biden for the difference, plus things overall were unimpressive especially relative to the previous boom decade once we pulled out of the Great Financial Crisis. And indeed, the author notes explicitly this is not the fault of either Biden or inflation.

If you put this all together, saying ‘inflation’ gave the voters a way to blame Biden for the decline in their real purchasing power that came in large part from the end of the stimulus, in addition to its other effects. You also see the partisan splits in perception of the economy, as you always do. In a world where a majority of voters dislike each party, and Biden was unpopular, it’s easy for people to use any excuse to think the economic times are bad.

Could Biden have done anything about all this? To some extent absolutely. There were any number of pro-growth policies he left on the table, and ways he actively got in the way of growth, and he overspent. But he was also, as many have noted, dealt a rather terrible hand on this, with the timing of the stimulus and resulting inflation. The fact that we outperformed almost all other countries economically during this period? Irrelevant to the median voter, who wouldn’t notice or care.

People think insurance should be some sort of magic thing, and complain when insurance companies price their products based on their costs plus a profit margin, and attempt to actually model the risks involved. Yes, insurance companies will act like scum to weasel out of paying if they can, but that’s a distinct issue.

The most pure version of this was an old Chris Rock routine where he says that they should call insurance ‘in case shit.’ And then he says, ‘if shit don’t happen, shouldn’t I get my money back?’ And the audience cheers. Except, well, yeah.

And no, this isn’t a weird Chris Rock thing. It’s common.

Spooky Werewolf Media: To be fair it’s not just that people don’t understand rudimentary aspects but that these things are propagandized and confused and marketed to hell and back by legions of bullshit artists.

Jeremy Kauffman: The degree to which society functions despite massive swathes not understanding even rudimentary aspects is a huge testament to capitalism.

(Nothing I write is ever investment advice, etc etc)

I write this note every so often, I think it’s important.

Duderichy: People vastly underestimate the alpha you have in your career!

If you’re in tech, you should be focusing on locking in a $500,000+ staff job instead of getting an extra $20,000 per year off your investments.

You can make a lot off your investments, but it’s hard to turn a lot of extra time into a lot of extra alpha, especially when your net worth is not large compared to your earning potential.

You do want to put in enough time to do something ‘reasonable’ but the answer (assuming you’re not planning for AGI) is plausibly things like ‘just find the right place to live, have an emergency savings account and then buy index funds, maybe buy index funds in industries that look promising and throw in some individual stocks and then forget about it.’

Beyond that, if your shower thoughts are focused on your investments, that will usually be a mistake until your investments are large compared to your income and career potential. Even when the amount of money at stake look large, that doesn’t mean the difference in alpha available from more attention is very high.

Insider trading increases liquidity from insiders that you don’t want to trade against. It decreases liquidity you do want from everyone else, who are subject to adverse selection.

In my experience, markets vulnerable to insider trading see their liquidity shrink dramatically – a clean example is if there is important unknown injury information in a sporting event, it all but kills the action until the information gets out, and markets for potentially fixed leagues are super thin.

Or: Who do you think is paying the insider traders their profits?

Insider trading might increase price efficiency, or it might not. Insiders have the incentive to fix prices, but others have far less incentive to do so. If I see Nvidia trading at 400 and my analysis says it should be 360 or 440, how do I know this isn’t because of insiders, and given that how do I dare trade? Or as they say in sports trading when the odds look weird: “Somebody knows something.” Maybe.

Whereas the insiders, this says, are against insider trading. Which I could see if it was due to it killing liquidity and ability to raise capital, but then that feeds back into the previous claim.

Alex Tabarrok asserts an evolving new consensus on the minimum wage, that effects are heterogeneous and take place on more margins than employment. I don’t know about the claim of an emerging consensus, but the claims themselves seem obviously true. In particular, those hurt by minimum wage laws are typically the worst off among us, with others largely unaffected, as economics 101 would suggest.

Whenever I see warnings about the national debt, like this one by Arnold Kling, they usually employ calculations like this one, where Kling quotes Cowen pointing the Rauh.

Joseph Rauh: if I use CBO projections to calculate the interest-to-revenue ratio, it reaches 22.9% by 2034.

The important warning that Kling is the latest to reiterate is that the bond market is currently in the good but unstable equilibrium of everyone expecting the government to pay its debts in valuable dollars, at least on a rolling basis. That means interest rates are reasonable. If we shift to the bad equilibrium, where investors do not assume this and demand higher prices, then we won’t be able to pay our debts without some form of large default, we will be vastly poorer, and there is no easy way back.

When we take on more debt, we raise both the danger that this happens, and the damage it would cause if it did happen. The good reason not to take on more debt is this tail risk.

There are remarkable similarities to things like AI existential risk – we know that going down this road will at some point start introducing steadily increasing risk of catastrophe, but until then we likely enjoy good times. There’s huge value in taking on a non-trivially risky amount of debt.

As we enjoy those good times, we don’t know what level of debt is how risky, with some even saying we can take on essentially unlimited debt and it’s fine, and every time we take on more debt people update that it’s safe to take on yet more debt – either you respond before the crisis, or you respond too late. As Kling puts it, ‘pretending there is no problem means that a sudden crisis is likely.’

How much debt is unsustainable? What is the actual current or anticipated debt burden? Tracking interest as a percentage of revenue is asking the wrong question.

There are essentially two questions that seem like they should matter here.

Can the good equilibrium be sustained? If we retain the ability to borrow at the risk-free rate of interest, or something not too far above it, can we keep the debt-to-GDP ratio from rising?

What will the bond market think is the bond market’s future answer to #1?

Japan, among other examples, shows us that we have a poor model of #2, as does the continued willingness to keep buying the debt of Argentina cycle after cycle. The coyote absolutely can sometimes run across thin air for longer than you think. That’s not the kind of thing I am in a position to model well, so I tend to focus more on #1.

According to Google, America pays about 3.35% on its monthly interest-bearing debt, and an average of 3.28% overall. Nominal GDP growth is higher than that, at 4.96%, similar to its historical average of 6.17% from 1948 to 2024. At current prices, the actual effective amount we pay in interest on the debt is less than zero – we could have debt of 100% of GDP, then have a primary deficit of 1.5% of GDP, and end the year with a better debt-to-GDP ratio than when we started.

That tells me that the answer here is more about demand for market priced safe government debt than it is about market price, similarly to the situation in Japan. My expectation is that the limiting factor here is that the ‘giant pool of money’ chasing safe assets is only so large. For now, demand exceeds supply by a lot, so we’re fine, and if someone dumps their supply that’s not an issue. If we try to borrow too much at once, we would exhaust demand, and have to adjust price in order to drum up more demand, not because of risk but because demand curves slope upward. So that’s what I would want to study, to find out where we should worry about potential breaking points.

Paying 5% of GDP in interest definitely sounds like a lot. It makes sense that everyone was actively concerned with the deficit and debt back then. But again, I’d be asking more about the steady-state cost of debt. What would it cost to make payments sufficient to prevent the debt from growing as a share of GDP, if the primary budget was in balance?

Which again brings us back to the question of multiple equilibria. The debt is fine, except for the risk that suddenly it very much isn’t. How far dare we go?

Jim Babcock explains how many memecoins and ‘market caps’ work, and how very often there is vastly less there than meets the eye. I find the whole thing deeply stupid, and if you propose I get involved with one I will absolutely block you.

Arguments and data in favor of the Peter Principle, that employees get promoted to their level of incompetence. To me this is one of those principles that is obviously true, the question is magnitude. The idea that ‘oh firms know about that, they’d successfully control for it so it wouldn’t happen at all’ is Obvious Nonsense.

Yay economies of scale. Much of what we consume has almost zero marginal product, and its marginal prices are usually falling rapidly to zero. An excellent reason to want more people around.

Since this section discusses various campaign proposals, I’ll reiterate:

I could not be happier with my decision not to cover the election outside of the particular areas that I already cover. I have zero intention of telling anyone who to vote for. That’s for you to decide.

All right, that’s out of the way. On with the fun. And it actually is fun, if you keep your head on straight. Or at least it’s fun for me. If you feel differently, no blame for skipping the section.

Last time the headliner was Kamala Harris and her no good, very bad tax proposals, especially her plan to tax unrealized capital gains.

This time we get to start with the no good, very bad proposals of Donald Trump.

The details of the announcement speech at the link are pure gold. Love it.

The economists, he said, told him he would get ‘a whole new workforce.’

Yes, that would happen, and now it’s time for Solve For the Equilibrium. What would you do, if you learned that ‘overtime pay’ meaning anything for hours above forty in a week was now tax free? How would you restructure your working hours? Your reported working hours? How many vacations you took versus how often you worked more than forty hours? The ratio of regular to overtime pay? Whether you were on salary versus hourly? What it would mean to be paid to be ‘on call,’ shall we say?

I used this question as a test of GPT-4o1. Its answer was disappointing, missing many of the more obvious exploitations, like alternating 80 hour work weeks with a full week off combined with double or more pay for overtime. Or shifting people out of salary entirely onto hourly pay.

I often work more than 40 hours a week for real, so I’d definitely be restructuring my compensation scheme. And let’s face it, the ‘for real’ part is optional.

This of course is never going to happen. If it did, it would presumably include various rules and caps to prevent the worst abuses. But even the good version would be highly distortionary, and highly anti-life. You are telling people to intentionally shift into a regime where they work more than 40 hours a week as often as possible, the opposite of what we as a society think is good. This is not what peak performance looks like, even working fully as intended.

Less fun Trump proposals are things like bringing back the SALT deduction (what, why, I am so confused on this one?) and a 10% cap on interest on credit cards. Which would effectively be a ban on giving unsecured credit cards with substantial limits to anyone at substantial risk of not paying it back or require other draconian fees and changes to compensate, and lord help us if actual interest rates ever approached 10%. Larry Summers notesthat this is a dramatic price cut on the order of 70% for many customers, as opposed to other proposed price controls that are far less dramatic and thus less destructive, so it would have far more dramatic effects faster. If payday loans are included they’re de facto banned, if not then people will substitute those far worse loans for their no longer available credit cards.

Then there’s ‘I’m going to bring down auto insurance costs by 50%’ where I could try to imagine how he plans to do that but what would even be the point.

Also there is his plan to ‘make auto loan interest tax deductible’ which is another fun one. Already car companies often make most of their money on financing. The catch is the standard deduction, which you have to give up in order to claim this. If the car loan is the only big item you’ve got, it won’t help you. What you need is some other large deduction, which will usually be a home loan. So this is essentially a gift to homeowners – once you’re deducting your mortgage interest, now you can also deduct your car loan interest. It makes no economic sense, but Elon Musk will love it, and it’s not that much stupider than the mortgage deduction. Of course, what we should actually do is end or phase out the mortgage deduction (as a compromise you could keep existing loans eligible but exclude new ones, since people planned on this), but I’m a realist.

Also there’s Trump’s other proposed huge giveaway and trainwreck, which is a quiet intention to ‘privatize’ Fannie Mae and Freddie Mac. I put privatize in air quotes because if you think for one second we would ever allow these two to fail then I have some MBS to sell you. Or buy from you. I’m not sure which. Quite obviously we are backing these two full on ride or die, so this would mean socialized losses with privatized gains and another great financial crisis waiting to happen.

As Arnold Kling suggests, we could and likely should instead greatly narrow the range of mortgages the government backs, and let the private sector handle the rest at market prices. When we back these mortgages, the subsidy is captured by existing homeowners and raises prices, so what are we even doing? Alas, I doubt we will seriously consider that change.

Another note on the unrealized capital gains issue is what happens to IP that pays out over time. For example, Taylor Swift suddenly owns a catalog worth billions, that could gain hundreds of millions in value when interest rates shift. Are you going to force her to pay tax on all that? How is she going to do that without selling the catalog? You want to force her to do that? Or do you want her to find a way to intentionally sabotage the value of the catalog?

We have some good news on the grocery price control front, as Harris has made clear that her plan would not involve global price controls on groceries and widespread food shortages. Instead, it will be modeled on state-level price gouging laws, so that in an emergency we can be sure that food joins the list of things that quickly becomes unavailable at any price, and no one has the incentive to stock up on or help supply badly needed goods during a crisis.

Tariffs are terrible, but not as bad as I previously thought, if there is no retaliation?

Justin Wolfers: Here’s a rule of thumb that Goldman draws from the literature:

Roughly 15% of a tariff is borne by exporters from the other country.

Another 15% results in compressed margins for American importers.

70% of the burden is borne by consumers paying higher prices.

The first 15% is indeed then ‘free money’ and the second 15% is basically fine. So if you were to use the tariff to reduce other taxes, and the other country didn’t retaliate, you’d come out ahead. You get deadweight loss from reduced volume due to the 70%, but you face similar issues at least as much with almost every other tax.

We use an advanced model of the global economy to consider a set of scenarios consistent with the proposal to impose a minimum 60% tariff against Chinese imports and blanket minimum 10% tariff against all other US imports. The model’s structure, which includes imperfect competition in increasing-returns industries, is documented in Balistreri, Böhringer, and Rutherford (2024). The basis for the tariff rates is a proposal from former President Donald Trump (see Wolff 2024). We consider these scenarios with and without symmetric retaliation by our trade partners.

Our central finding is that a global trade war between the United States and the rest of the world at these tariff rates would cost the US economy over $910 billion at a global efficiency loss of $360 billion. Thus, on net, US trade partners gain $550 billion. Canada is the only other country that loses from a US go-it-alone trade war because of its exceptionally close trade relationship with the United States.

…

When everyone retaliates against the United States, the closest scenario here to a US-led go-it-alone global trade war, China actually gains $38.2 billion.

Noah Smith does remind us that no, imports do not reduce GDP. Accounting identities are not real life, and people (including Trump and his top economic advisor) are confusing the accounting identity for a real effect. Yes, some imports can reduce GDP, in particular imports of consumer goods that would have otherwise been bought and produced internally. But it is complicated, and many imports, especially of intermediate goods, are net positive for GDP.

The context of his comment was a hearing where people quite insanely proposed to ban lap infants on flights, which the FAA has to fight back against every few years by pointing out that flying is far safer than other transportation.

So such a ban would actively make us less safe by forcing people to drive.

A comment points out Jeremy is playing loose here: 4% is who listed this as the primary reason for being out of the labor force. A lot more did have difficulty.

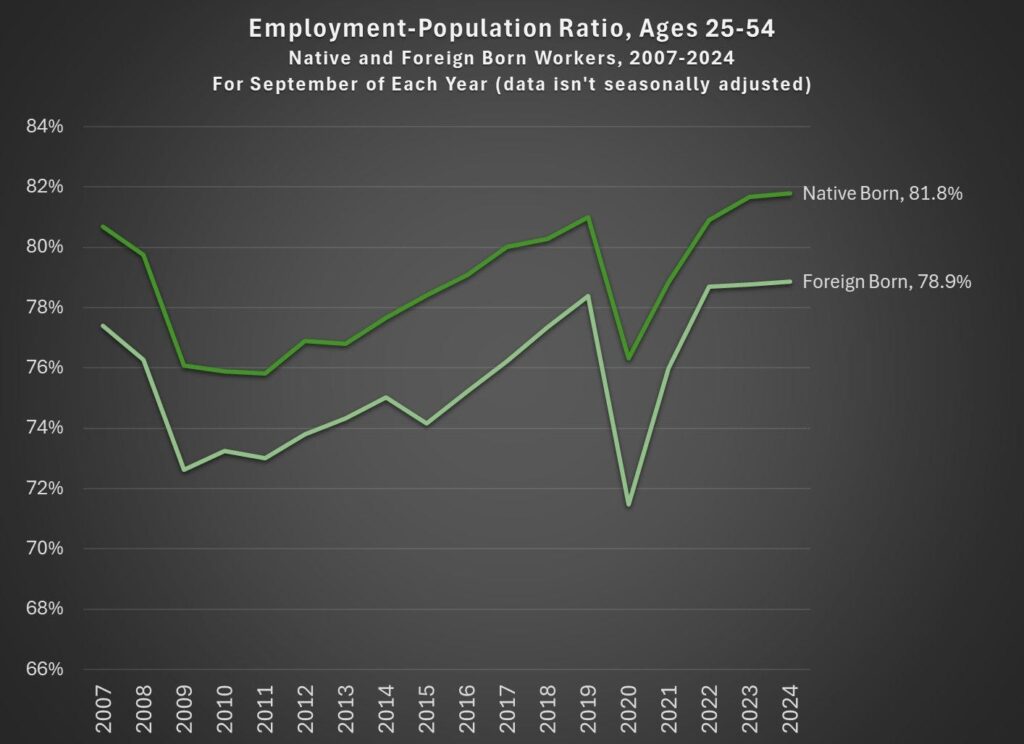

Jeremy: Also, the prime-age employment rate is near all-time highs — some men aren’t in the LF, this is true, but women are employed at by far the highest rate ever. This suggests that the number of jobs isn’t the problem, but something (or things) are making men drop out (see above).

And the prime age employment rate is highest for native-born workers

Yes, a lot of those jobs are terrible. But that has always been true.

Kalshi will pay 4.05% on both cash and open positions, which will adjust with Fed rates. That’s a huge deal. The biggest barrier to long term prediction markets is the cost of capital, which is now dramatically lower.

Election prediction market update: As I write this, Polymarket continues to be the place to go for the deep markets, and they have Trump at 55% to win despite very little news. So we’ve finally broken out of the period where the market odds were strangely 50/50 for a long time, likely for psychological reasons driving traders. The change is also reflected in the popular vote market, with Trump up to 31% there, about 8% above his lows. Nate Silver’s predictions have narrowed, he has Harris at 51% to win, down from a high of 58%.

The move seems rather large given the polls and lack of other events. My interpretation is that the market is both modestly biased in favor of Trump for structural reasons (including that it’s a crypto market and Trump loves crypto) and that the market is taking a no-news-is-good-for-Trump approach.

I haven’t heard anyone think of it that way, but it makes sense to me. Consider the debate. Clearly the debate was good for Harris, including versus expectations. But also the debate was expected to be good for Harris, so before the debate the polls were underestimating Harris in that way. One could similarly say that Harris generally has more opportunity to improve and less chance of imploding or having health issues over the last two months, so her chances go down a little if Nothing Ever Happens.

As many have pointed out, there is little difference between 44% Harris at Polymarket, and 51% Harris at Silver Bulletin. Even if one of them wins decisively, it won’t mean that one of them is right and the other wrong. To conclude that you have to look at the details more carefully.

We’ve gone over this before but it bears repeating, and I like the way this got presented this time around. How bad are our marginal tax rates for those seeking to climb into the middle class, once you net out all forms of public assistance, taxes and expenses?

Brad Wilcox: Truly astonishing indictment of our welfare policies fr @AtlantaFed. A single mother in DC can make no gains, financially, as her earnings rise from $11,000 to $65,000 because benefits like food stamps & Medicaid phase in/out as her income rises. Terrible for work/marriage.

Andrew Jobst: Talked to someone who lost their job in the GFC (highly educated, driven, professional credentials). Wanted to start her own business. Commented about how demoralizing it was to hustle all day to earn another dollar, only for her unemployment benefit to drop by a dollar.

Benefits are not ‘as good as cash’ so the problem probably is not quite as bad as ‘100% effective marginal tax rates from $10,000 in income up to $65,000’ but it could be remarkably close, especially in places with high additional state taxes. Can you imagine what would happen if you took a world like this, and you stopped counting tips as taxable income, as proposed by both candidates?

Effectively, you’d have a ~100% tax rate on non-tip income, but 0% on tips (and Trump would add overtime). Until you could ‘escape’ well above the $65k threshold, basically everyone would be all but obligated to fight for only jobs where they could get paid in these tax-free ways, with other jobs being essentially unpaid except to get you to the $10k threshold.

Given these facts, what is remarkable is how little distortion we see. Why isn’t there vastly more underground economic activity? Why don’t more people stop trying to earn money, or shift between trying to earn the minimum and then waiting to try until they’re ready to earn the maximum, or structuring over time?

My presumption is that this is because the in-kind benefits and conditional benefits are worth a lot less than these charts value them at. Cash is still king. So while the effective rate is still quite high, we don’t actually see 100% marginal tax rates.

If you want more income, Tyler Cowen suggests perhaps you could work more hours? A new estimate says 20% of variance in lifetime earnings is in hours worked, although that seems if anything low, especially given as Tyler points out that working more improves your productivity and human capital.

Tyler Cowen: In the researchers’ model, 90% of the variation in earnings due to hard work comes from a simple desire to work harder. Note again this is an average, so it does not necessarily describe the conditions faced by, say, Elon Musk or Mark Zuckerberg.

In my experience, vastly more than 20% of my variance in income comes from the number of hours worked and how hard I was working generally. One could draw a distinction between hours worked versus working hard during those hours. I’d guess the bigger factor is how hard I work when I’m working, but the times I’ve succeeded and gotten big payoffs, it wouldn’t have happened at all if I hadn’t consistently worked hard for a lot of hours. The time I wasn’t able to deliver that effort, at Jane Street, it was exactly that failure (and what caused that failure) that largely led to things not working out.

Working hard also applies to influencers. In this job market paper from Kazimier Smith, he finds that the primary driver of success is lots of posting. Sponsored posts grow reach the same as regular posts, which is nice work if you can get it, although this results likely depends on influencers selecting good fits and not overdoing it, and on correlation, where if you are getting sponsorships it is a sign you would otherwise be growing.

The abstract also introduced the question of focus and audience capture. Influencers and other content creators have to worry that if they don’t give the people what they want, they’ll lose out, and I’ve found that writing on certain topics, especially gaming, creates permanent loss of readers. I’d love to see the proper version of that paper too.

Since we’ve now had some major storms, it’s time for another round of reminding everyone that laws against ‘price gouging’ are a lot of why it we so quickly run out of gas and other supplies in emergency situations. Why would you stock extra in case of emergency, if you only can sell for normal prices? Why would you bring in extra during an emergency, if you can only sell for normal prices?

Dr. Insensitive Jerk: Our relatives in the Florida evacuation zone just told us I-75 is a parking lot, and no gasoline is available.

Do you know why no gasoline is available? Because of price-gouging laws.

Pointing this out provokes a predictable emotional response from adult children. “He should give me gas cheaply! He should store an infinite amount of gasoline so he can fill up all the hoarders, and still have gas left for me, and he should do it for the same price as last week!”

Now when Floridians need gasoline desperately, they can’t buy it at any price, because other Floridians said, “It’s cheap, so I might as well fill the tank.”

People outside Florida with tanker trucks full of gasoline might have considered helping, but instead they said, “I won’t risk it. If I charge enough to make it worth my while, I will be arrested and vilified in the press.”

But at least the Floridians won’t have to lie awake in their flooded houses worrying that somebody made a profit from rescuing them.

Alas, the Bloomberg editorial board will keep on writing correct takes like ‘Price Controls Are a Bipartisan Delusion’ (the post actually downplays the consequences in a few cases, if anything) and we will go on doing it.

Maxwell Tabarrok: High prices during emergencies aren’t gouging – they’re bounties for desperately needed goods. Like a sheriff offering a big reward to catch a dangerous criminal, these prices incentivize the entire economy to rush supplies where they’re most needed.

With two major hurricanes in the last couple of weeks, “price gouging” is in the news. In addition to it’s violent name, there are good intuitive reasons to dislike price gouging.

But imagine if you were the sheriff of Ashville, NC, and it was your job to get more gasoline and bring it into town.

You might offer a bounty of $10 a gallon, dead or alive.

That’s a lot more than the usual everyday bounty, but this is an emergency.

Prices aren’t just a transfer between buyer and seller.

They’re also also a signal and incentive to the whole world economy to get more high-priced goods to the high-paying area; they’re a bounty.

The last thing you’d want if you were the sheriff is a cap on the bounty price you’re allowed to set.

High prices on essential goods during an emergency are WANTED posters, sent out across the entire world economy imploring everyone to pitch in and catch the culprit.

The difficulty that many people may have in paying these higher prices is a serious tragedy, and one that can be alleviated through prompt government response e.g by sending relief funds and shipping in supplies. But setting prices lower doesn’t mean everyone can access scarce and expensive essential goods. In an emergency, there simply aren’t enough of them to go around.

Setting low prices might mean the few gallons of gas, bottles of water, or flights that are available are allocated to people who get to them first, or who can wait in line the longest, but it’s not clear that these allocations are more egalitarian.

These allocations leave the central problem unsolved: A criminal is on the loose and a hurricane has made it difficult to get these goods to where they’re needed.

When there’s an emergency and a criminal is on the loose, we want the sheriff to set the bounty high, and catch ‘em quick. High prices during other emergencies work the same way. Let the price-system sheriff do his work!

Scott Sumner points out that customers very much prefer ridesharing services that price gouge and have flexible pricing to taxis that have fixed prices, and very much appreciate being able to get a car on demand at all times. He makes the case that liking price gouging and liking the availability of rides during high demand are two sides of the same coin. The problem is (in addition to ‘there are lots of other differences so we have only weak evidence this is the preference’), people reliably treat those two sides very differently, and this is a common pattern – they’ll love the results, but not the method that gets those results, and pointing out the contradiction often won’t help you.

Chinese VC fundraising and VC-backed company formation has fallen off a cliff, after China decided they were going to do everything they could to make that happen.

Bill Gurley: Many in Washington are preoccupied with China. If this article is accurate, the #1 thing we could do to improve US competitiveness, would be to open the door much more broadly & quickly to skilled immigration. Give these amazing entrepreneurs a home on US soil.

It’s important to note these are private VC funds and VC-backed companies only. This is not the picture of all new enterprise in China. There are plenty of new companies.

According to FT, venture capital has died because the Chinese government intentionally killed it. They made clear that you will be closely monitored, your money is not your own and cannot be transferred offshore, your company is not your own, the authorities could actively go after the most successful founders like Jack Ma, that you are to reflect ‘Chinese values’ or else. Venture capital salaries are capped.

What is left of venture is often suing companies to get their money back, so the government doesn’t accuse them of not trying to get the money back on behalf of the government. New founders are required to put their house and car on the line.

The advocates of Venture Capital and the related startup ecosystem present it as the lifeblood of economic dynamism, innovation and technological progress. If they are correct about that, then this is a fatal blow.

Often we hear talk about ‘beating China,’ along with warnings of how we will ‘lose to China’ if we do some particular thing that might interfere with venture capital or the tech sector. Yet here we have China doing something ten or a hundred or a thousand times worse than any such proposals. Yet I don’t expect less worrying about China?

One perspective listing what 2% compounding annual economic growth feels like once you get to your 40s. It is remarkably similar to my experience – I look around and realize that the stuff I use and value most is vastly better and cheaper, life in many ways vastly better, things I used to spend lots of time on now at one’s fingertips for free or almost free.

We argue that workers must take costly actions (“conflict”) to have nominal wages catch up with inflation, meaning there are welfare costs even if real wages do not fall as inflation rises.

We study a menu-cost style model, where workers choose whether to engage in conflict with employers to secure a wage increase.

…

We conduct a survey showing that workers are willing to sacrifice 1.75% of their wages to avoid conflict. Calibrating the model to the survey data, the aggregate costs of inflation incorporating conflict more than double the costs of inflation via falling real wages alone.

Matt Bruenig: Also worth considering the degree to which “conflict costs” constitute another of the frictions that prevent job-switching (people don’t like upsetting their boss/colleagues), which again points towards collective bargaining as important and a limitation of anti-monopsony.

I got a job once that I left after 6 weeks because I got an unexpected offer that paid about $20k more per year and boy did I have to hear what a piece of shit I was from the person who hired me in the first job. It’s as if they had never even read the textbook.

Matt Yglesias: This resonates with me as I ask myself why I re-upped my Bloomberg column contract at the same nominal salary without even attempting to negotiate for a higher fee.

Except I have seen unions, and whatever else you think of unions they do not exactly minimize such conflicts, instead frequently leading to deadweight losses including strikes. And I have no doubt that inflation substantially increases the average costs of such conflicts.

The reason a worker would pay to avoid conflict with the boss is partly it is unpleasant, partly The Fear, and partly because it can result in anything from turning the work situation miserable up through a full ‘you’re fired,’ or in the union case a strike. At minimum, it risks burning a bunch of goodwill.

Also Matt should realize that when you take a new job after six weeks and quit, you have imposed rather substantial costs on your old employer. During those six weeks, you were probably a highly unproductive employee. They spent a lot of time hiring you, training you, getting you up to speed, and then you burned all that effort and left them in another lurch.

Of course they are going to be mad, although the bigger the gap in offers the less mad they should be. We’ve decided that the employee doesn’t strictly owe the employer anything here, it’s a risk the employer has to take, but at minimum they owe them the right to be pissed off – you screwed them, whether or not it was right to do that.

Another way to look at this is that the decline in real wages is a cost, which then often means other costs get imposed, including deadweight losses like switching jobs or threatening to do so, in order to fix it, but that as is often the case those new costs are a substantial portion of the original loss.

There are also the actual real losses. This is especially acute in situations that involve wages being sticky downwards, or someone is otherwise ‘above market’ or above their negotiating leverage. For example, when I joined [company], I was given a generous monthly salary. I stayed for years, but that number was never adjusted for inflation, because it was high and I needed my negotiating points for other things – I didn’t want to burn them on a COLA or anything.

Often salary negotiations happen at times of high worker leverage, when they have another offer or are being hired or had just proven their value or what not. Having to then renegotiate that periodically is at minimum a lot of stress.

As one commenter noted, sufficiently high inflation can actually be better here. If there’s 2% inflation a year, then you’re tempted to sit back and accept it. If it’s 7%, then you have a fairly straightforward argument you need an adjustment.

But this policy was sufficiently known and reliable that it resulted in absolutely massive tax evasion, as in 95% of people earning under $2,000 a year flat out not bothering to file. Needless to say, at that point you might as well set the tax for such people to $0 and tell them they don’t need to file.

John Horton: If you listen, insurance companies are giving you solid, data-driven advice about stuff not to do or buy—don’t own a pit bull, don’t have a trampoline, don’t under-water cave dive, don’t own a “cyber” truck…

what’s kind of nuts is that when instead of just quoting you a higher price, they explicitly just will not cover it. To me, that suggests they think adverse selection is a problem. It’s not *justthat pit-bulls are natural toddler-eaters, they think you’re a reckless idiot and a higher price just increases the average idiocy of the customers, with predictable results

Gwern: Or they don’t have enough data.

The problem is, insurance companies only need correlates. So none of that is good advice about stuff you should do – unless you are planning to starting to transition to a woman because of lower insurance rates for women on many things…?

Robert Parham: Upon inspection, it seems like a externality issue. The cybertruck is so tough that any accident with it leaves the truck unscathed while totalling the other car. The Insurance company is liable for the totalled car, hence the decision.

Insurance is indeed pretty great for things like internalizing that your cybertruck would be very bad for any other car that got into an accident with it. The problem is that when you price out trampoline insurance, a lot of this is that people who tend to buy trampolines are reckless, so you don’t know how much you should avoid owning one.

I even wonder if ‘arbitrary’ price differentials would be good. If you charge less for insurance on houses that are painted orange than those painted green, and someone still wants to insure their green house, well, do they sound like responsible people?

As the tech job market continues to struggle, I’m seeing more threads like this asking if it’s time to reevaluate career and college plans based around being a software engineer. My answer continues to be no. Learning how to code and build things is still a high expectancy path.