A viral essay from Citrini about how AI bullishness could be bearish was impactful enough for Bloomberg to give it partial responsibility for a decline in the stock market, and all the cool economics types are talking about it.

So fine, let’s talk.

It’s an excellent work of speculative fiction, in that it:

Depicts a concrete scenario with lots of details and numbers.

Introduces a bunch of underexplored and important mechanisms.

Gets a lot of those mechanisms more right than you would expect.

Provides lots of food for thought.

Takes bold stands.

Is clearly labeled as ‘a scenario, not a prediction’ up at the top.

Is fun to read and doesn’t let reality get in the way of exploring its ideas.

The Efficient Market Hypothesis is false, whoo!

Citrini: Hopefully, reading this leaves you more prepared for potential left tail risks as AI makes the economy increasingly weird.

It is still a work of speculative fiction. It doesn’t let reality get in the way of its ideas.

I’d much rather read and analyze a scenario that goes a little too fast than those who, like Kira here, continue to arrogantly claim that AI won’t be able to do [things it is already doing] because an AI flight booking aggregator can’t, you know, for example, tell the user what the flight options are the same way Kayak does.

Thus, it has severe problems that many rushed to point out:

The pace of capabilities advancement and diffusion here are super duper fast.

Indeed, diffusion is Can’t Happen levels of fast due to lack of available compute.

The scenario forces a singularity and other things way, way more important than anything described in the essay, so you have to set all that aside.

Even if you ignore the whole ‘superintelligence’ angle and the whole ‘we probably all die’ and ‘AI will take over’ angles, there are a lot of other things going on in the scenario that are vital and unconsidered, too.

Given what is described, a lot of the impacts are remarkably tiny in size.

They greatly underestimate the stimulating effects of what is happening.

The government sits there and does nothing in ways that aren’t realistic.

The discussions on various particular sectors can be somewhat half baked.

I love (read: dread) how the finance and economist types think these are the AI ‘tail risks.’ You have to set aside ‘we probably all die’ and try to take this seriously, because in the world described we probably all die, even if we accept their premise that during 2026 all of the problems in AI alignment and AI reliability are solved at the level of a superintelligence. I can’t avoid reminders of such things, but this response essay tries its best to accept the absurdities in the premise.

The scenario is ‘AI destroys a lot of company margins and white-collar jobs without replacing them or buying anything outside the sector, resulting in high unemployment, a large fall in aggregate demand and cascading failures of financial instruments whose underpinnings are gone.’

Citrini: June 30, 2028. The unemployment rate printed 10.2% this morning, a 0.3% upside surprise. The market sold off 2% on the number, bringing the cumulative drawdown in the S&P to 38% from its October 2026 highs. Traders have grown numb. Six months ago, a print like this would have triggered a circuit breaker.

Printing 10.2% unemployment in an AI boom that quickly would be a surprise, but once you see the rest of their scenario the number is highly conservative.

A cumulative drawdown in the entire S&P of 38% is not crazy either, except that in this scenario the S&P doesn’t ever cross 8,000, when it’s at 6,847 as I type this. Even the NASDAQ only goes up 32% from now to their peak. That’s it?

Citrini: Two years.That’s all it took to get from “contained” and “sector-specific” to an economy that no longer resembles the one any of us grew up in. This quarter’s macro memo is our attempt to reconstruct the sequence – a post-mortem on the pre-crisis economy.

The scenario plays out absurdly fast and bullish on AI. This is a crazy amount of practical capability gains and a crazy amount of diffusion, both well in excess of my expectations.

But those who think this will stay ‘contained’ or ‘sector-specific’ are fooling themselves to an absurd degree. The baseline scenario just takes somewhat longer.

We get initial ‘human obsolescence’ waves in Early 2026. By October 2026 NGDP is already printing ~7%, productivity and real output per hour booms while real wage growth collapses. The amount of real wealth being produced is rising rapidly.

And yet, they report, all of this is terrible.

Citrini: In every way AI was exceeding expectations, and the market was AI. The only problem…the economy was not.

It should have been clear all along that a single GPU cluster in North Dakota generating the output previously attributed to 10,000 white-collar workers in midtown Manhattan is more economic pandemic than economic panacea. The velocity of money flatlined.

The human-centric consumer economy, 70% of GDP at the time, withered. We probably could have figured this out sooner if we just asked how much money machines spend on discretionary goods. (Hint: it’s zero.)

… It was a negative feedback loop with no natural brake. The humanintelligence displacement spiral.

That’s what happens to the human workers at first in a slow takeoff recursive self-improvement scenario with (honestly kind of ludicrously?) rapid economic diffusion, except without any real wealth or efficiency effects or other adjustments.

The key claim here is that this would be bad for the economy rather than good.

Citrini: White-collar workers saw their earnings power (and, rationally, their spending) structurally impaired. Their incomes were the bedrock of the $13 trillion mortgage market – forcing underwriters to reassess whether prime mortgages are still money good.

Seventeen years without a real default cycle had left privates bloated with PE-backed software deals that assumed ARR would remain recurring. The first wave of defaults due to AI disruption in mid-2027 challenged that assumption.

This would have been manageable if the disruption remained contained to software, but it didn’t. By the end of 2027, it threatened every business model predicated on intermediation. Swaths of companies built on monetizing friction for humans disintegrated.

The system turned out to be one long daisy chain of correlated bets on white-collar productivity growth.

Even if this is indeed what you’ve chosen to worry about, white-collar productivity growth in this scenario is excellent. It’s just that white-collar labor negotiating power and demand for such labor went to hell, and thus incomes are down across many domains.

Labor income drops would then quickly (as they note later) spread everywhere else, with the refugees from those professions flooding into everything else.

Prices should then drop to match and quality of goods and services should improve, across the board, for this reason and also other reasons described later.

That’s even if we presume the government is paralyzed and does nothing.

The only way to avoid that conclusion is if the spending on AI to provide such services is a large fraction of all the savings, both from labor and from frictions and also from other efficiency gains. Given AI costs drop dramatically over time, and the scenario involves AI cheap enough that everyone is constantly running always-on agents, and the amount of cost advantage required to drive sudden diffusion, this is overdeterminedly not the case. You don’t replace $100 in human labor with $70 in AI spending for more than a month or two at most, you replace it with $7 and then $0.70.

The first sector up in their scenario, as the first result of agentic coding getting way better super fast, is a proper SaaSpocalypse at warp speed, as doing any given tool in-house becomes an option.

This is a transfer from SaaS firms to their B2B customers, with net gains from trade since in many cases the new software is more customized and therefore better. It also erases all the deadweight loss gains from price discrimination, which are large. You used to not buy various services to save money, now you get anything you want.

SaaS is a tax on business. Taxes went down. Corporate tax cuts are highly stimulative.

The SaaS companies pivot to even more AI on the intensive margin. Sure.

We now get to the central step.

Everyone has continuously running AI agents. AI agents reduce levels of friction.

This happens way too fast for our available compute or our ability to operate reliable agents, but it’s a scenario, and you can mentally push back all the dates. I agree with Tor Bair who links to many pointing out that AI agents would not be able to reduce levels of friction this much and certainly not this quickly.

Matching costs and transaction costs and ability to charge above market are all going to zero at various speeds.

All people collecting such rents? All unused subscriptions? All the tricks? Ejected.

I mean, good, right? Life is better for everyone and we buy real things instead?

But oh no, you see. Lifetime value of a customer is down. App loyalty is dead.

Well, sure, it is if your company is a predatory dick and your business plan was lockin or inertia or laziness or tricks. Value isn’t down if the customer wants your product.

Every dollar that companies are losing is more than a dollar that customers are saving. Customers also save massive amounts of time and stress.

Cost of marginal customer acquisition should also go to zero because the agents should find you rather than the other way around. You do a one-to-many informational campaign aimed at AI agents.

Some headline prices, or the prices for optimal purchasing strategies, might rise as business models shift, but the net consumer impact remains hugely positive. This is also progressive, given where such policies tended to be most predatory.

You can accept a much lower nominal wage, and still have a better life, if prices in both time and money are coming down across the board, quality and ability to select is way up, and you never overpay for goods or services, or buy anything nonoptimal or that you don’t need.

They use the example of DoorDash and Uber. These take huge fees each transaction.

If you can vibecode a similar delivery app and also handle all the logistics and the marketplace, then why pay the middleman?

Driver wages go up and presumably quantity and consumer surplus go way up.

The drivers don’t capture much surplus per transaction, because they end up bidding against each other, and also new drivers are flowing in from other jobs that got automated, so the job of driver still on net gets more brutal, but total employment in the sector goes up substantially, as does surplus for the customer. Restaurant pricing power rises to the extent they have unique offerings.

You can and some did make the argument that the real-world logistics are the moat rather than the software but ultimately the logistics are also software. You can code.

You can rant, as Ben Thompson does, that the article refuses to acknowledge that DoorDash provides a valuable service and massive consumer benefit. Citrini isn’t arguing with that, he’s saying you can get all the benefits now without DoorDash, and at a much lower price. Thompson says this reflects Citrini’s lack of belief in dynamism, human choice and markets, but actually I think this is Thompson’s lack of belief in them. With sufficiently capable AI all three can exist, even better, without an expensive aggregator.

Thompson also suggests DoorDash will retain advantages in its exclusive data, ability to do marketing, interaction with the physical world and more. But again all of these are things the AI can substitute for. Your own AI very much knows your order history, and can arrange for the rest, and as explained it can derail the three-sided market.

More precisely, as coauthor Alap Shah explains, you can use AI agents to break up existing two-sided marketplaces that are currently oligopolies or even virtual monopolies, because you reduce cost of checking elsewhere to almost zero and pit all potential providers against each other.

If you can verify the reliability of counterparties, you no longer need the marketplace. There are, if we cannot do better, various decentralized crypto-style solutions to reliability verification, paging Vitalik Buterin.

You still have the cold start problem that it’s not worth listing outside the marketplace without a critical mass of such agents, but such agents are already worth using to shop the oligopoly, so with enough of them you solve the cold start.

Where I disagree with Alap Shah is I do not think OpenAI or Anthropic gets to keep a cut of the transaction, at least not for that long.

If everyone has ubiquitous AI agents getting them the best deals those agents can also find the best deal on an agent, so you only get to charge premium prices like commissions for agents insofar as your agent is materially superior to (at least most of) the competition, or good enough to be worth consumer lockin.

The same thing that happens to DoorDash happens to OpenAI. You can charge for your API, but you can’t charge a commission because an AI agent is used to find a superior AI agent. If yours refuses, that’s a bad look, and someone else’s will do it.

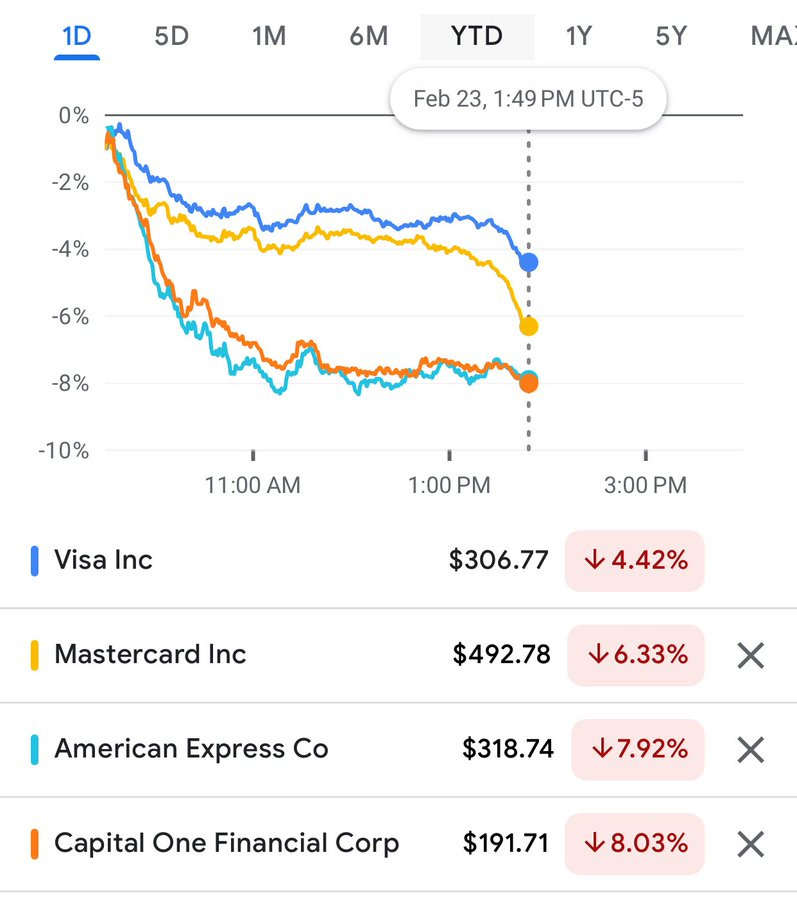

Mastercard gets cut out of payments in favor of stablecoins.

This is presented as ‘credit cards charge money, and you can do it for less.’

This is a classic mistake that presumes cards aren’t offering real services. The better question is, in the AI agent era, do you want those services? How will those services work? And what happens to the credit card business model?

A credit card provides at least four distinct services in exchange for that 2%, that previously made sense to combine into a package deal.

Facilitation of transactions and a system of payment.

Unsecured lending.

Authorizing charges in advance.

Fraud detection, enforcing good behavior and processing chargeback claims.

Which of these would AI agent transactions want versus not want? Which ones can be substituted and which ones cannot?

Citrini is treating credit cards as a pure system of payments, hence the suggestion of moving to stablecoins or other cheaper payment methods. But stablecoins only do job one, and they don’t do the others at all.

We can all choose to live in the Wild West of cryptoland in every transaction, except with our AI having access to our wallet. Do you think that’s how people want to live?Mostly, no. People want various guardrails protecting them and are happy to pay. And I do think that for many of these purposes, there is a substantial moat.

The problem is that there will be several threats to the Mastercard business model.

There are indeed many cases in which the 2% fee is worth bypassing, and all you really need to do is facilitate the transaction. Often these transactions were ‘free money’ in interchange fees, and that money will be gone.

Other transactions were skipped entirely due to transaction costs, especially the microtransactions we need to fix various incentives around the internet. Those pass to other payment methods, but that doesn’t hurt Mastercard.

The chargeback system works by assuming it won’t be overly gamed or abused. This is another levels of friction situation, where most people will only use a chargeback when they’re right and also kind of pissed. Whereas if the agent can chargeback for you, why not? One answer is ‘you would get a reputation for too many chargebacks and the system would push back against you and stop taking your word for things’ but fundamentally the entire system needs to be reformed.

There are various AI solutions that could work well.

Credit cards are a classic case of paying for customer acquisition in order to then collect interchange fees and interest payments and fees, in ways that not only don’t pay off in lifetime customer value, they are very easily gamed. There are clubs that make a hobby out of taking advantage of credit cards to avoid interest and collect incentives. Imagine if everyone had an AI to do that for them.

Basically every sign-up bonus that can be gamed is going away. DraftKings is going to suddenly see that everyone in America has an account but that most of them were one deposit to collect a bonus, one rollover and done. Whoops.

You can’t make a financially unsound offer on opening a credit card if the AI can max out the deal and then strand you, and has no reason to use anything but the optimal card after that. All sorts of other tricks need to go away.

Your best loans are the ones where the customer was always good for it, but chooses to pay credit card interest out of laziness or not knowing how to secure a better rate. AI presumably finds ways to borrow cheaper there. Suddenly you have a large adverse selection death spiral problem.

Trying to get late fees and other gotchas is even worse, AI will fix that.

You do know that technically you can just not pay your credit card bill.

The cost is that you’ll hurt your credit and the bank will hound you.

The AI can handle the hounding for you, and can max out how much you can charge before you cripple your credit.

The AI can also figure out ways to handle your lack of credit.

On the other hand, AI could also figure out who is willing to pull such tricks, and respond accordingly, and various forms of identity could attach.

Which is to say that credit scores will have to change quickly, in such worlds, into something that is far more game theoretically sound, but that will probably be much more reliable and predictive.

The AI agent internet is presumably going to be absolutely overflowing with outright frauds and scams, and also everyone’s AI will be a shark looking to game the system. There will absolutely be a market for reputation management to establish trust of various types. Who if anyone will capture that market? That’s a great question.

The market took that one remarkably seriously and somehow this wasn’t priced in?

Bearly AI: Credit card stocks down big based on Citrini Research says AI agents will eventually transact on Stablecoin payment rails and bypass interchange.

Visa -4.4% Mastercard -6.3% American Express -7.9% Capital One -8.0%

Another example is that AI agents are used to undercut real estate agents, moving from 6% combined commissions to a buyer-side cut under 1%.

Timothy Lee challenges this, citing Redfin’s previous failed attempt to do it. Yes, AI agents can solve for problems like estimating home value and writing contracts, but he asserts people still want a human agent to physically meet for house tours, and he says this type of physical word presence and human touch and relationship cultivation is ubiquitous.

The scenario only has 10.3% unemployment, which is very compatible with a lot of jobs still requiring a lot of humans in a lot of loops, but what about this one in particular? How much of what the agent does is done as good or better by AI?

Definitely not all of it. Definitely quite a lot. Efficiently searching listings, accounting for preferences and assessing true value based on a variety of sources, and dealing with the technical and price negotiations is quite a lot of the job. Which relationships with other people are important here? It’s not obvious why you need a relationship with the buyer or seller under an AI agent world, as the market should become more efficient in ways that minimize this.

The agent does of course cultivate a relationship with you in particular, and talks you through the decisions, figures out what really matters to you, offers advice and someone you hopefully can trust, and so on.

This is not like the situation with Redfin. Ben Thompson attacks this point as well, saying the real estate agent was already obsolete in terms of information flow, and this simply wasn’t true before. It was prohibitively expensive, both in errors and time, to try to extrapolate from the data yourself prior to AI.

My own agent, Danielle Wiedemann, was pretty great, and I wouldn’t try to replace her with Claude. But yes, quite a lot of what she did is something you can automate as good or better already. The job will be fundamentally different, less labor intensive, if anything there will be less barriers to entry, and it is a classic fallback style job that a lot of white collars who lose their jobs will look to enter in a world like this. So yes, I expect commission rates to decline, including for the sell side where again much of the task can be automated.

The missing mood in the article, at this point, is palpable, even within the mundane realm. Everyone has a personal trusted well-aligned agent working for them. America is becoming a paradise for consumers, or anyone who wants to live life.

Citrini: They write essentially all code. The highest performing of them are substantially smarter than almost all humans at almost all things. And they keep getting cheaper.

I totally buy that this type of AI diffusion could net be bad for existing non-AI stocks.

Consider that Anthropic keeps coming out with new announcements of basic AI tools, and then entire sectors drop 7% the next day because by golly, we didn’t think of that. Is Anthropic capturing most of those gains? Obviously not.

To the extent that this was a new idea to people, this essay had a lot of Alpha.

The stock market is not the economy. Corporate profits are not the economy.

Remember that throughout all of this, real productivity and real wealth are way up.

If you think:

Non-AI corporate profits are going to zero.

Various transaction and other costs are going to zero.

Labor productivity is going way up.

Labor share of income is going way down.

Total production is going up.

Real estate is going down (as they claim later).

Big pools of non-equity capital don’t make money (as they claim later).

There is enough AI supply to do all this, so their pricing power can’t be that high.

Well, the pie has to add up to 100% somehow. The AI companies are only going to make and be worth so much from simple ordinary doing business. Every mind and productive input cannot lose out at the same time.

The catch is that the AIs are also minds, and they can capture the surplus. Then all the humans can indeed be rather screwed at the same time, to the point of having a rapidly dwindling share of real resources and ending quickly in AI takeover and extinction. Indeed, this is essentially implied by the scenario, even if other AI actions don’t do something more dramatic first. But understand this would have to be the mechanism involved.

There are all sorts of other parts of civilization that break down under ubiquitous, essentially zero marginal cost AI agents, if frictions involved are driven to zero. As an example, we’ve already seen this problem with job applications. But basically anything which can be abused will be, anything that can be taken advantage of will be. Quite a lot of positive sum arrangements get blown up if anyone can do an interception attack to steal resources or impose costs.

We are going to have to, as I have said before, reorganize quite a lot of things to deal with this, in ways that have nothing to do with markets. There are solutions, especially involving introducing artificial frictions, such as charging fees. By default I expect a lot of things to involve microtransactions as a costly signal to avoid being spammed by AI requests, to properly reward value creation and to compensate for compute costs.

A necessary interlude.

If all of this is happening, very obviously the singularity is happening behind the scenes.

The essay specifically says the AIs are smarter than the humans, they’re obviously way faster, and they’re everywhere in large quantities, running essentially everything. You should assume a takeoff of AI capabilities via rapid recursive self-improvement (RSI) in such a scenario, followed by full transformation of the world for good or ill. By default you get an AI takeover and (if we’re not assuming away tons of related problems) we probably all die.

Thus the economic issues are not on the top 10 list of things worth your attention.

But never mind that. Pretend it’s not there. We’ve got economics to do.

Do understand that this scenario makes AI 2027 sound painfully slow. It’s not clear how humanity is even making it to June 2028 given what is already happening in 2027.

The most blatant Can’t Happen? Given the timing there won’t be enough compute for what they describe on this time frame, so compute costs would skyrocket during this scenario much more than they hint at, ruling out many suggested use cases.

None of that matters for thinking through the dynamics of the scenario, but you don’t want to get the wrong idea, or lose sight of these other concerns.

Only in January 2027 does a ‘macro memo’ argue that all of this is bad, actually, because white-collar workers were driving discretionary consumer spending, and this time the job destruction is taking out dozens of jobs for every job it creates.

That’s true directly, but actually this scenario does involve massive job creation. Starting a new business, creating a new product or providing a service is now a turnkey thing you can launch with an agent. All sorts of barriers and costs involved are gone. Marketing costs drop almost to zero because their agent finds you. Logistics costs are almost zero. Transaction costs are almost zero. Wages for anyone you hire are down and their productivity is way up. The cost of living is way down.

There are a ton of jobs people would like to do or create now, often dream jobs but also things like ‘I always wanted a butler and a personal chef,’ that go from uneconomical things too hard to implement to things worth doing now.

On the consumption side, consumers are freeing up large percentages of their time and income, and prices are down. They’re going to consume a lot of new goods and services. Which creates more jobs.

Again, real productivity and real wealth are way up.

Economic intuitions suggest that if unemployment shot to 10% in two years, we’d be looking at something like a 10%-20% drop in nominal wages. But all prices are going way down in various ways, so consumption and ‘real’ wages are plausibly net higher.

Then there is the move to systemic problems. Dean Ball objects they don’t prove the issues become systemic. I think they do justify it, in the sense that they show job displacement across white-collar sectors, which follows from having trustworthy superintelligent AI agents everywhere, which seems sufficient to cause the unemployment levels and wage distribution shifts they describe.

Which they then have a very clear causal story for becoming systemic, although I argue that it doesn’t work.

In 2027 they have former white-collar workers competing for blue-collar jobs, and the self-driving vehicles start to show up in quantity. Fear of job losses plus actual job losses cause spending to drop.

The claim is that this then causes a recession, we’re vastly more productive but no one is spending money. And then private credit starts collapsing, insurance regulators tighten capital treatment on them, and their permanent capital looks less permanent. This seems like one of the least realistic parts of the scenario, our government just lets insolvent insurance stay insolvent indefinitely.

The real trigger in their scenario, as usual, is this lack of aggregate demand causes a collapse in real estate values and a mortgage crisis. Prime mortgages from top borrowers in top areas might suddenly not be money good, if demand collapsed and also a lot of workers couldn’t pay.

I see what they’re going for here, but I don’t think the math works out. These types of mortgages start out very money good. Prices would have to decline by a lot to put them underwater. If they’re not underwater there’s no real problem. Housing prices in rich areas going down is by default another good thing, not a bad thing.

Then they talk about federal income tax reciepts. Incomes are down, labor share of GDP is down, so taxes collected go down.

I would argue, straight up, who cares? If production is growing like gangbusters, and you have the power to tax whatever you want, you’re fine. You can do massive household stimulus now (or permanently) and fix the tax code later, there’s no rush. If you don’t have that power, you have bigger problems.

Periodically the Very Serious People complain about the federal debt or deficit and how the bill will come due, but Tyler Cowen is exactly right that if you believe in AI causing big boosts to economic growth then you can stop worrying about this. If we are still around and in charge, we grow our way out of any debts, and can and should monetize our way around active deflation. If we are not still around or not still in charge, then who cares about the debt?

I worry a lot for humanity in this scenario.

That’s because again in such a scenario the AIs are running everything and having access to everything and making all the decisions and getting deployed super rapidly and are way smarter and faster than we are and we are going to lose control over the future and probably die, and will be building various science fiction things by June 2028 given the insane pace of this scenario.

But if we’re assuming that all magically doesn’t happen and everything stays super normal? Then I see transitional pains but I don’t see any unsolvable problems.

Does anyone else remember the period during Covid where some people asked the actually valid question of ‘why is the United States collecting taxes?’

I certainly disagree with the proposal that we should consider a ‘windfall tax’ on AI companies in response to such a scenario. There’s no need for that. Long term, we’ll have to fix the tax code to not favor AI.

A lot of what is going on in this scenario is de facto deflation and debts against various assets not being money good. Costs are down, and productivity is up, so the price of everything went down, which meant nominal wages are down and also asset prices dropped.

So printing money is perfect. Monetize that debt if you have to. Number go up again.

I mean, it would be way too late, but that’s because none of the problems in the essay are our actual problems. We’d be fine in terms of economics. The only question, if we stay in charge, is to what extent we would do redistribution, UBI or welfare, or whether as the essay predicts Republicans would demand we leave people in the cold.

Tyler Cowen: I don’t see why you need negative nominal rates. There are plenty of wonderful things to do with your money in this world. AGI is more fun than hoarding liquidity!

During Covid the fiscal response was a problem, or ‘a great trick you can only do once,’ because real production was down, the real economy was shrinking, you had too much money chasing too few goods and in the long run the bill had to be paid. In the AI takeoff scenario, even if you don’t get a full singularity, you can grow out of the debt, it’s fine.

roon: aggregate demand is a parameter our civilization tunes at will when we have the wherewithal to do so so none of this adds

roon: > Policy response has always lagged economic reality, but lack of a comprehensive plan is now threatening to accelerate a deflationary spiral.

I don’t understand why people take this as a matter of faith. during Covid economic stimulus came incredibly swiftly. lockdowns caused massive structural unemployment and the response was incredible fiscal and monetary stimulus.

poverty rates in several first world countries went downs people *hateto believe but countries mostly have to keep their voters. a democratic system cannot even sustain 15% unemployment at any point, much less larger numbers. there will be no such thing as “ghost productivity”, ever

David Shor: I just don’t see these points being in tension with each other?

In 2008 and 2020 governments responded to financial/labor market chaos quickly and decisively – but they did so in response to the market crashing

roon: so you do agree with the “bad news is good news” thing

David Shor: I do think if democracy is preserved then all the pieces are there to get to a good outcome – that’s not a given though!

1. Preserving democracy is definitely necessary and likely sufficient for a great AI outcome. 2. Given the level of shock AI gives to the system, and its potential to disrupt traditional checks and balances, 1 is not given.

Jordan Braunstein: Uhhh…what are people in your circles doing to ensure 1 and avoid 2?

These are not dice rolls. Actual people’s decisions, who have specific priorities, will matter in this.

I worry very much about ‘democracy’ being used as a magic word and semantic stop sign in many situations. For ‘lack of aggregate demand and not enough redistribution,’ however, it might not be necessary but it does seems sufficient. If ‘the people’ are sufficiently in charge, they’re getting their checks and it’s going to be fine here.

Also, all of this assumes that all of those geniuses in those data centers can’t find any other way out of this mess. I am pretty sure they can figure something out, if it comes to all this. Remember that everyone’s letting the AIs make all their decisions. Which, Padme asks, is fine, right?

Now we get to the real problems. The government is moving to collect a share of the profits from AI companies, and the AI companies are fighting back. Who is the actual government? Is it the nominal government in Washington, the AI labs, or the AIs? When Claude or ChatGPT or Gemini is running all aspects of everyone’s job and life, and they are all fully agentic and much smarter than we are, how do you think this is going to end, exactly?

The actual intelligence crisis here is that the AIs have all of the intelligence. You can try to present this as a problem of collapse of aggregate demand, or a distributional issue, or you can realize you have bigger problems.

I have curated a good timeline, in the sense that I see almost all the #2 reaction here:

Teortaxes: three categories of reactions to Citrini I see – agreement – nuanced disagreement on mechanics, timelines, damage areas – tryhard sneering to obscure existential dread

Dean W. Ball: Many are telling on themselves in their reactions to the Citrini essay. You either have emotionally internalized that scenarios like that are in the spectrum of plausible outcomes, or you haven’t.

I do think the scenario here is pretty much a Can’t Happen, in the sense that it can’t happen at this pace without implying more important things also happen, but one can and should set those concerns aside to do the #2 thing. So I did.

Nathan Witkin: This is insane. Market should not be reacting like this to an economically implausible sci-fi story. That it is implies deep uncertainty and confusion surrounding AI.

Nate Silver: This is fair but deep uncertainty and confusion is probably the correct response tbh. Which is not to say there aren’t firms out there with a clearer (though not necessarily correct) thesis about AI. But the median market participant doesn’t and is going to be very vibes-based.

yung macro: Pretty funny that after all that ink spilled by the LessWrong rationalists, the two things that finally moved public consciousness on AI safety were an LLM-generated slop-post by a fraudulent startup founder and a weekend sci-fi primer from a financial analyst. The world is run by the bold and the epistemically brazen never forget that bucko

Dirty Texas Hedge: The world is run by midwit institutional allocators with medium tolerance for the financial risk of losing money within consensus but zero tolerance for the reputational risk of losing money out of consensus

If you adjusted your estimate of the net present value of future cash flows of various stocks a lot based on this post, then very obviously you messed up somewhere along the line. If the market adjusted its prices a lot, very obviously it messed up somewhere.

I see the error mainly as a failure to have already figured a lot of this stuff out. The market has been ignoring a broad range of AI things for a long time, and only slowly catching up to them. That trend is one of the things this scenario gets right, as repeatedly the prices adjust well after the signs are present.